Lecture 4

Externalities

September 5, 2025

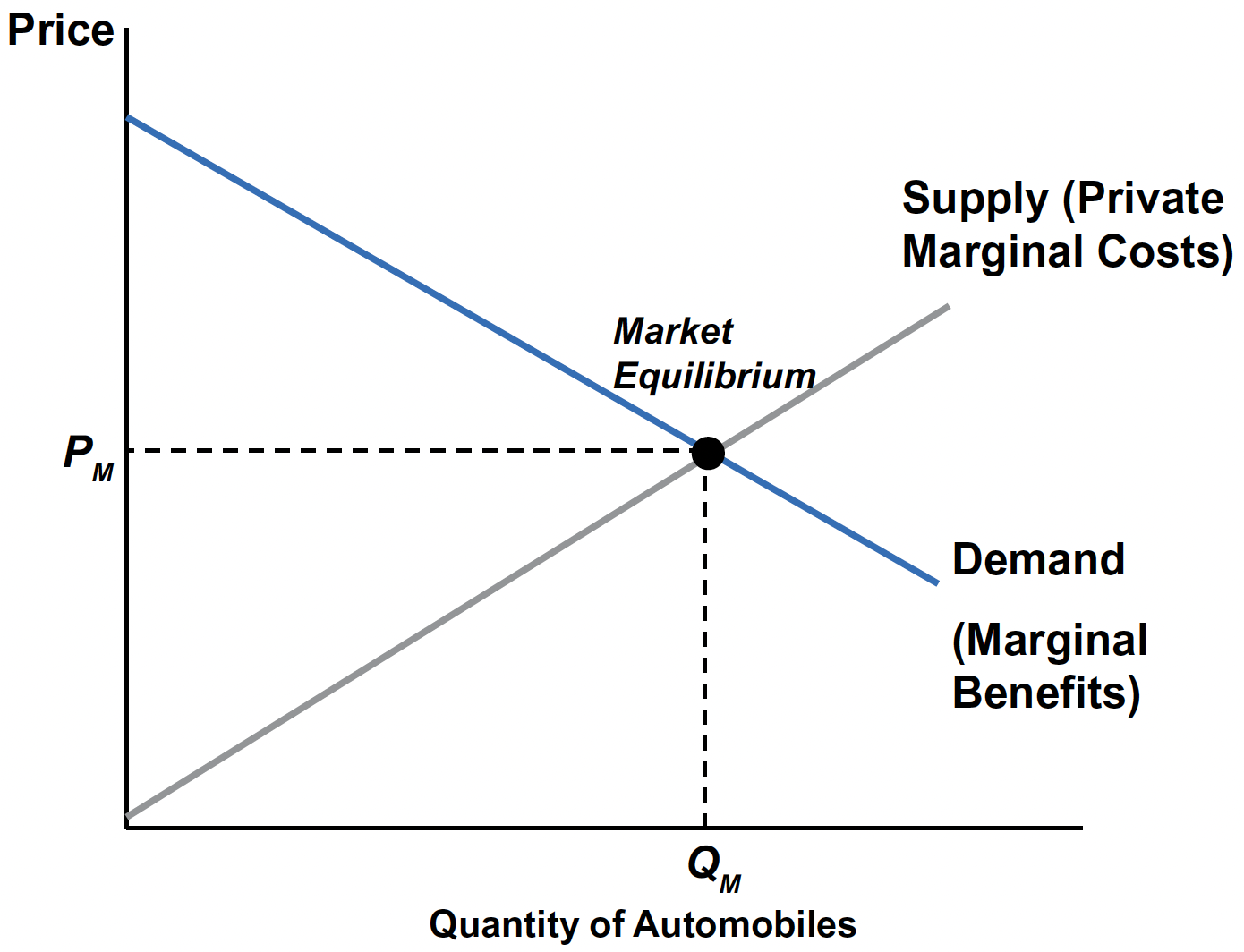

The Market for Automobiles

- Supply curve ≈ PMC: private marginal cost of producing one more unit (labor, materials, energy, etc.).

- Demand curve ≈ PMB: private marginal benefit (consumers’ willingness‑to‑pay for one more unit).

- Market equilibrium \((P_{M}, Q_{M})\) is efficient only if PMC = SMC and PMB = SMB (i.e., no externalities).

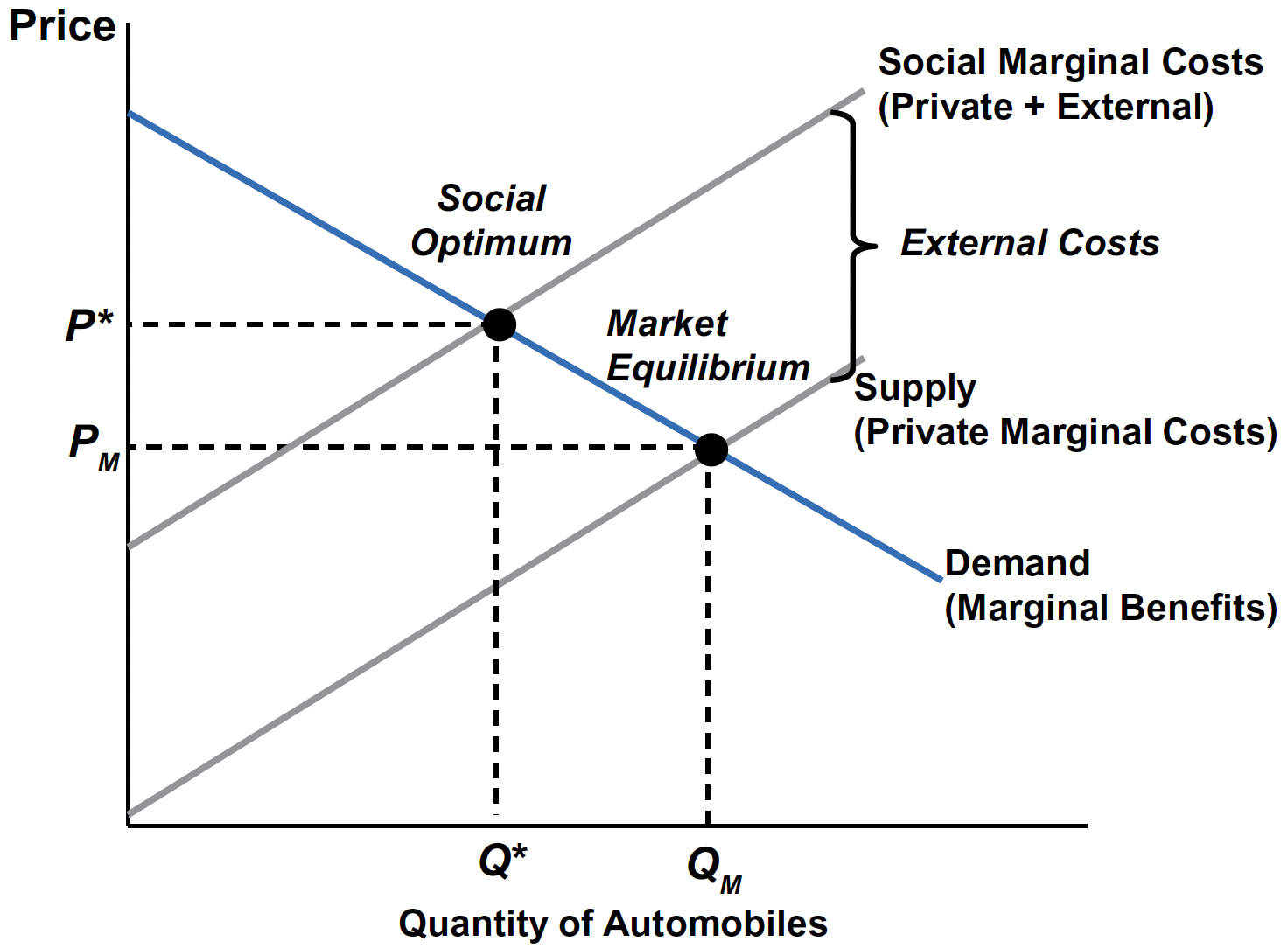

The Market for Automobiles with Negative Externalities

- SMC = PMC + EMC, where EMC is the external marginal cost.

- Typically, EMC rises with output when pollution/congestion intensify.

- SMC lies above PMC by the vertical distance equal to EMC.

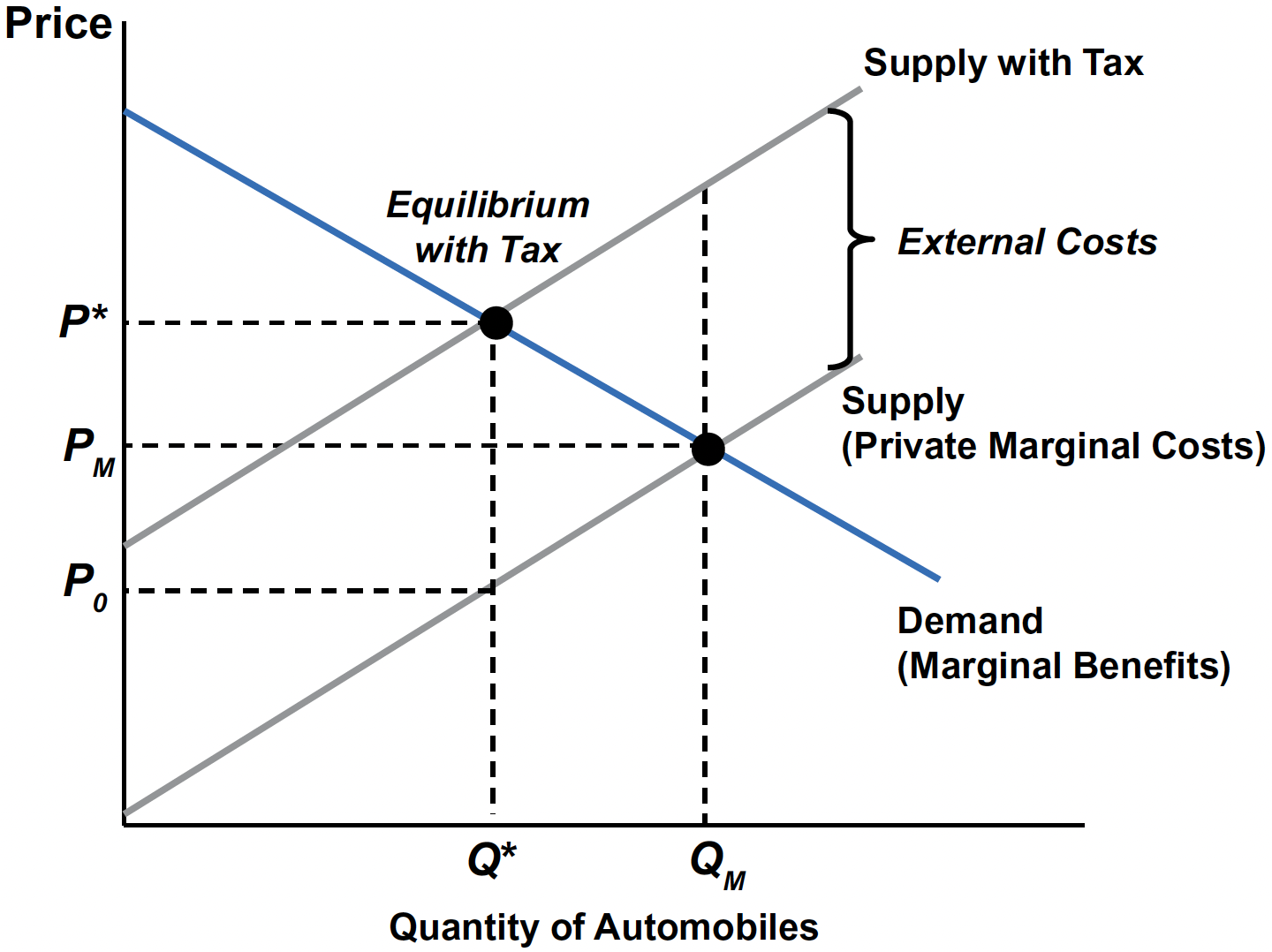

Automobile Market with Pigovian Tax

- Impose a per‑unit tax \(t\) equal to EMC at \(Q^{*}\).

- Effect: raises firms’ private marginal cost so the effective supply coincides with SMC.

- New equilibrium: \((P^{*}, Q^{*})\)—the socially efficient outcome.

- Set the right rate

- Target the per-unit external damage at \(Q^{*}\) so PMC + \(t\) = SMC.

Economic Tax Incidence & Elasticities

- Consumer incidence: the amount of the tax revenue paid by consumers

- Producer incidence: the amount of the tax revenue paid by producers

Who Pays? Economic Incidence & Elasticities

- Who pays more?

- The less elastic (steeper) side of the market bears more of the tax.

- The less elastic (steeper) side of the market bears more of the tax.

- The claim “firms pass it all on” is generally false; division is empirical and depends on elasticities.

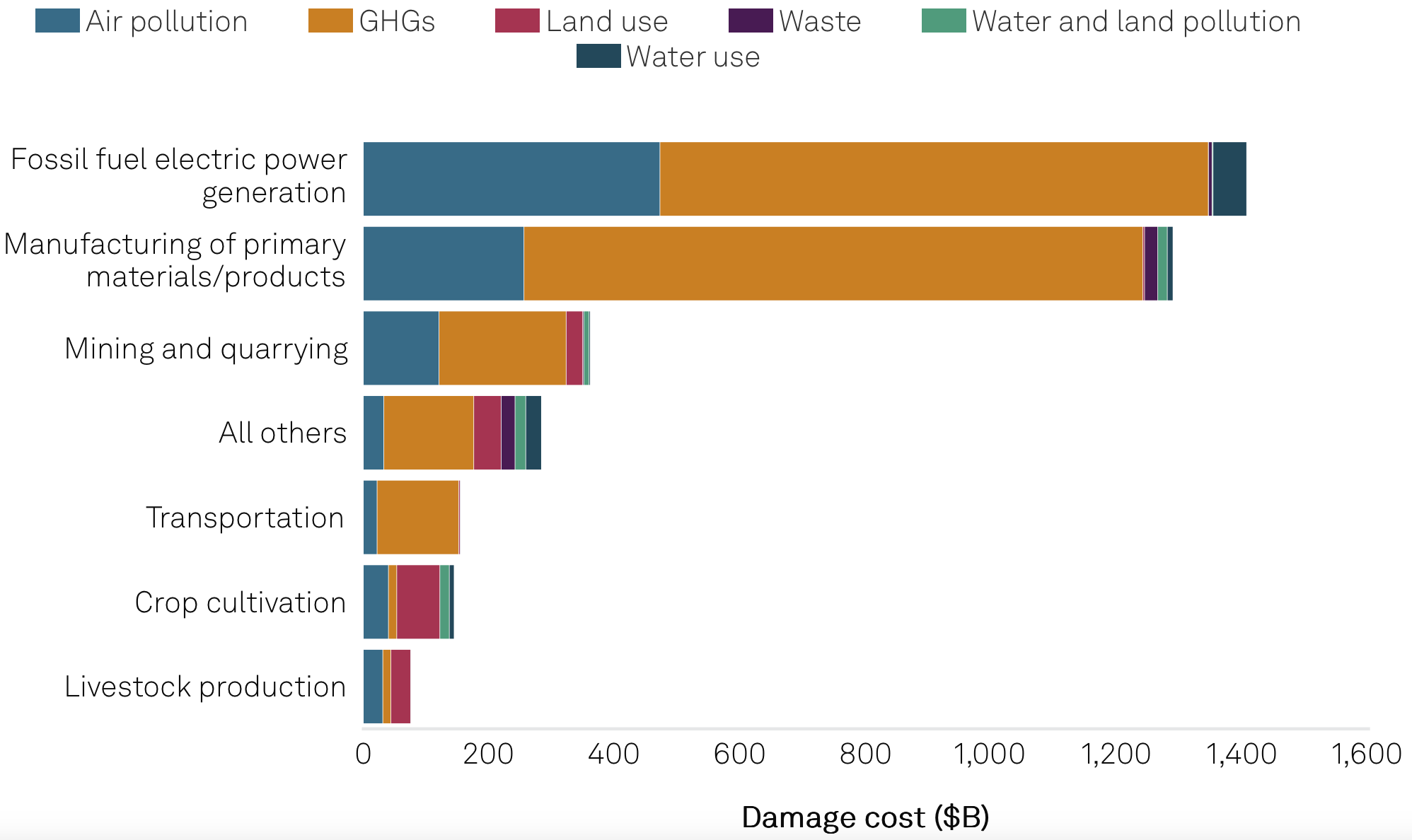

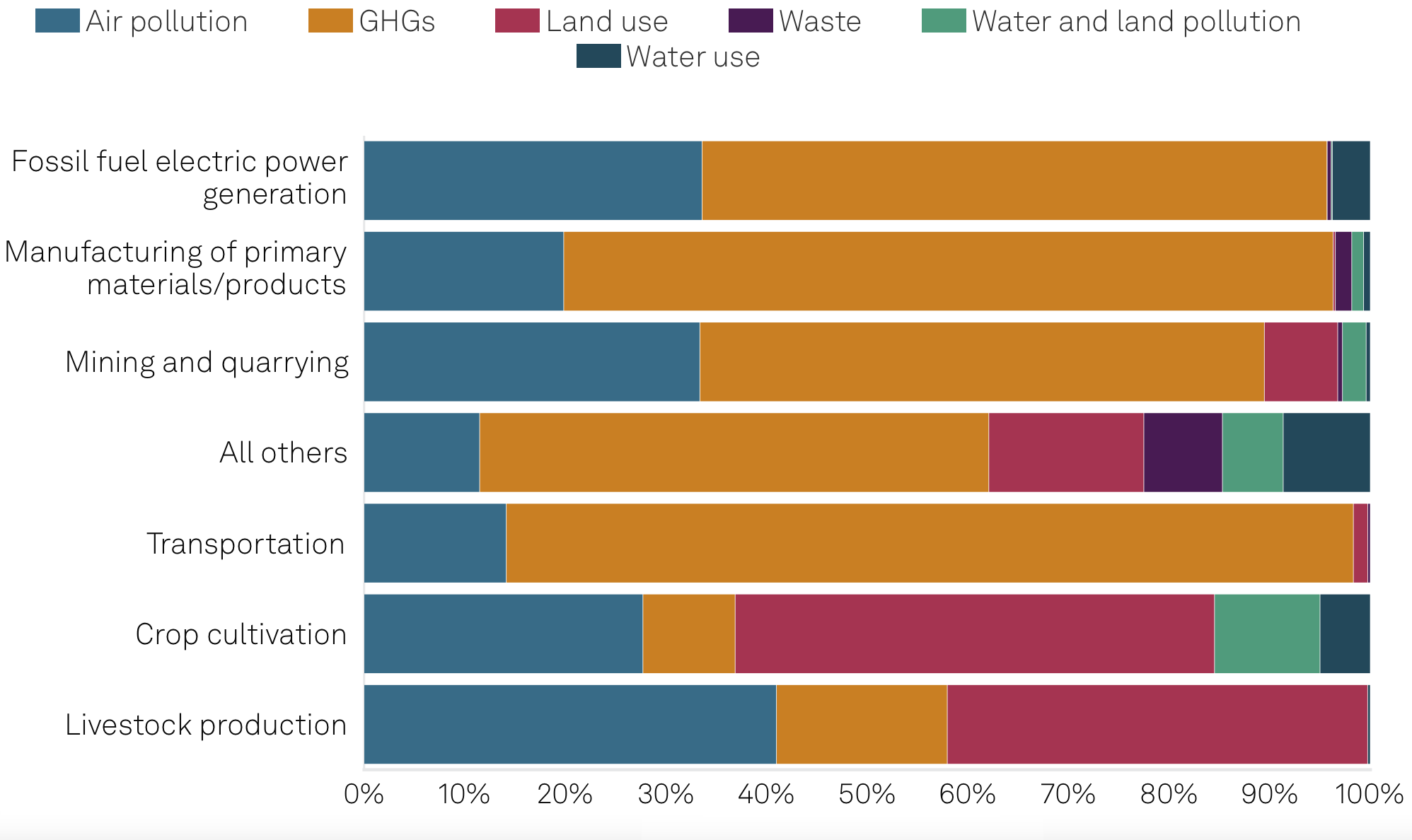

The Top Externalities of the Global Market

Environmental damage costs generated by companies in the S&P Global Broad Market Index by sector group in 2021.

The Top Externalities of the Global Market

Source: S&P Global Sustainable1.

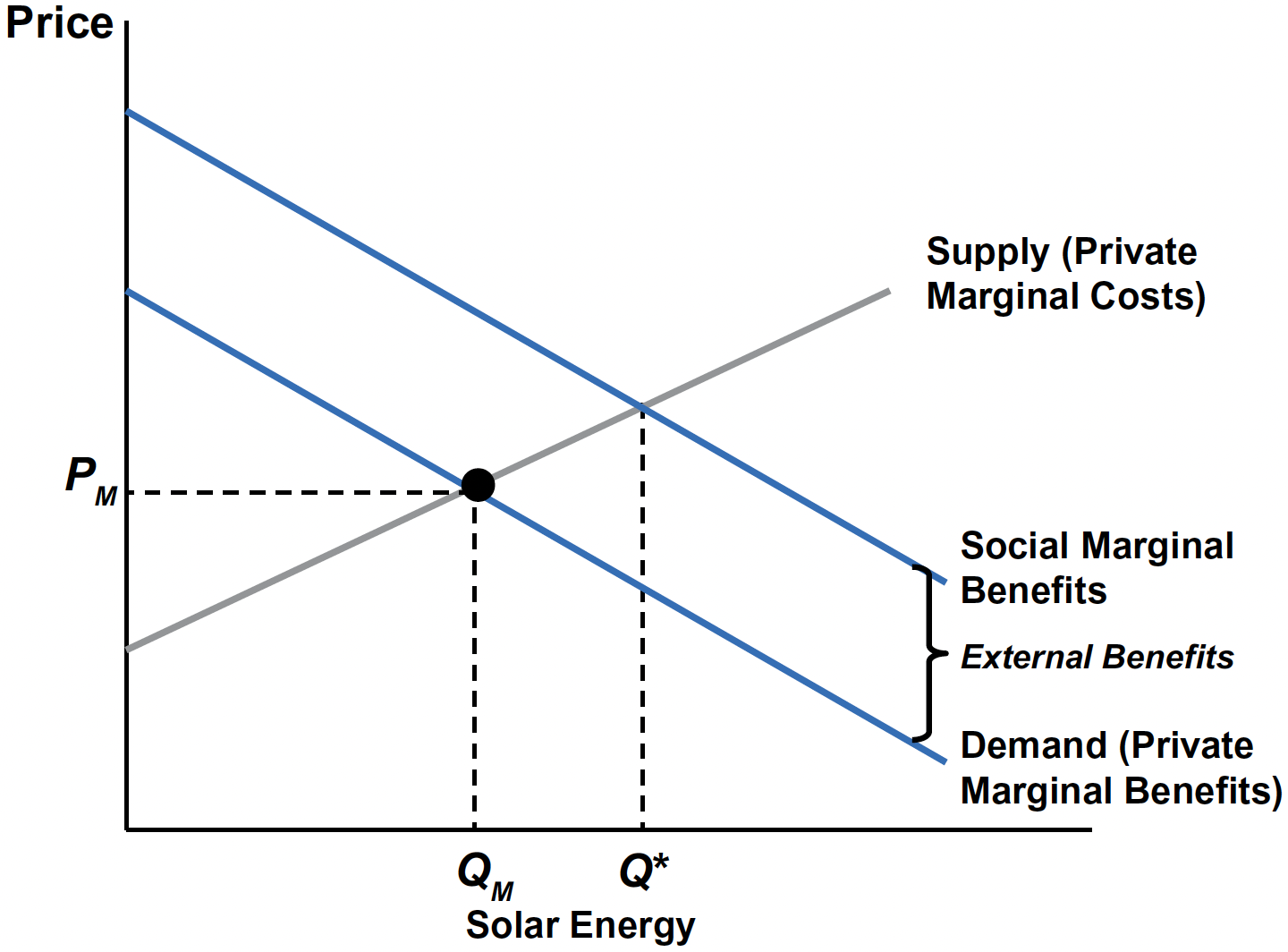

The Market for Solar Energy

- SMB = PMB + EMB, where EMB is external marginal benefit.

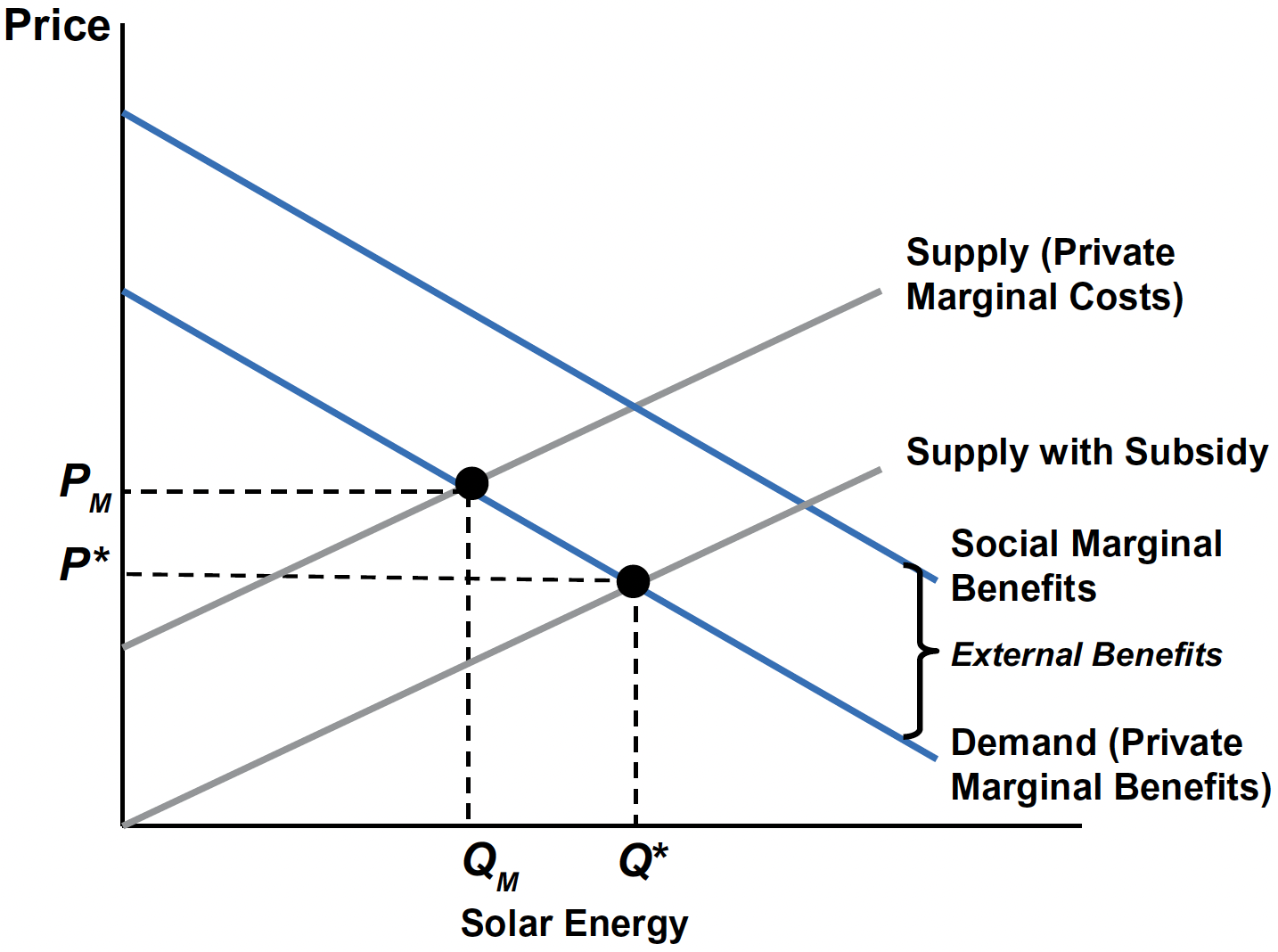

The Market for Solar Energy with a Subsidy

- A producer subsidy of \(s\) per unit lowers effective marginal cost (downward supply shift).

- A consumer subsidy (e.g., tax credit) raises effective willingness‑to‑pay (upward demand shift).

- Correct subsidy aligns the market with \(Q^{*}\) where SMC = SMB.

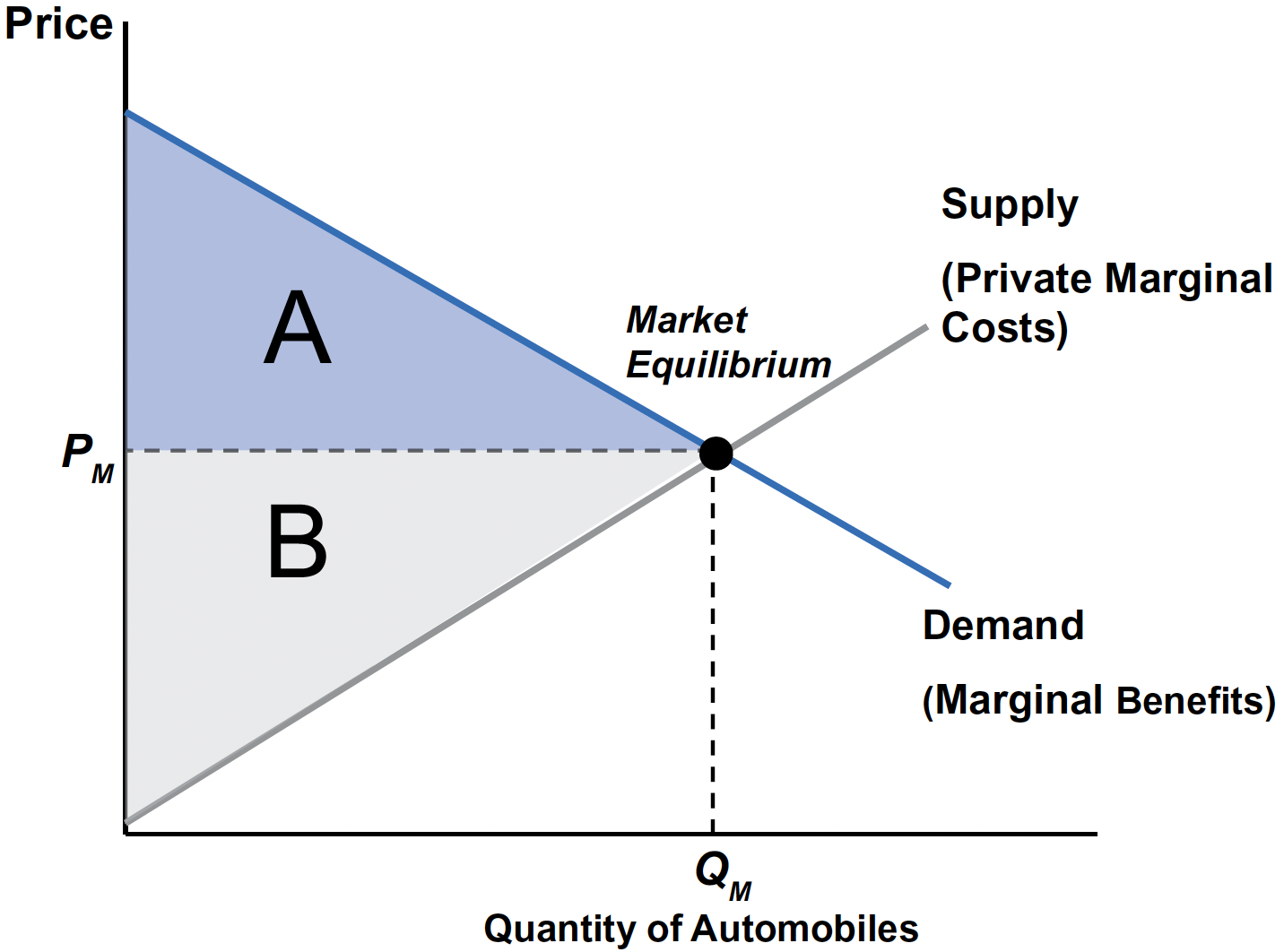

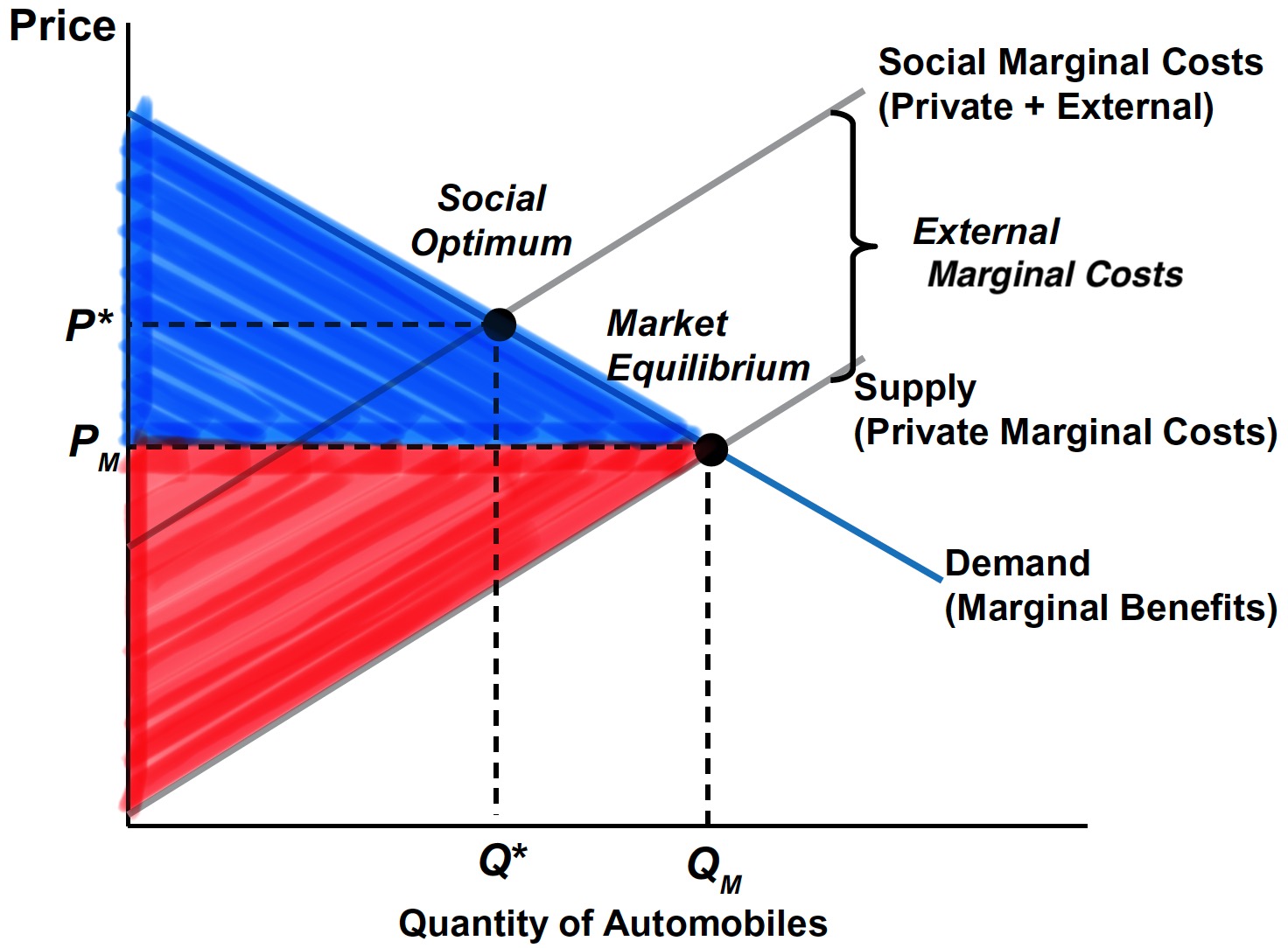

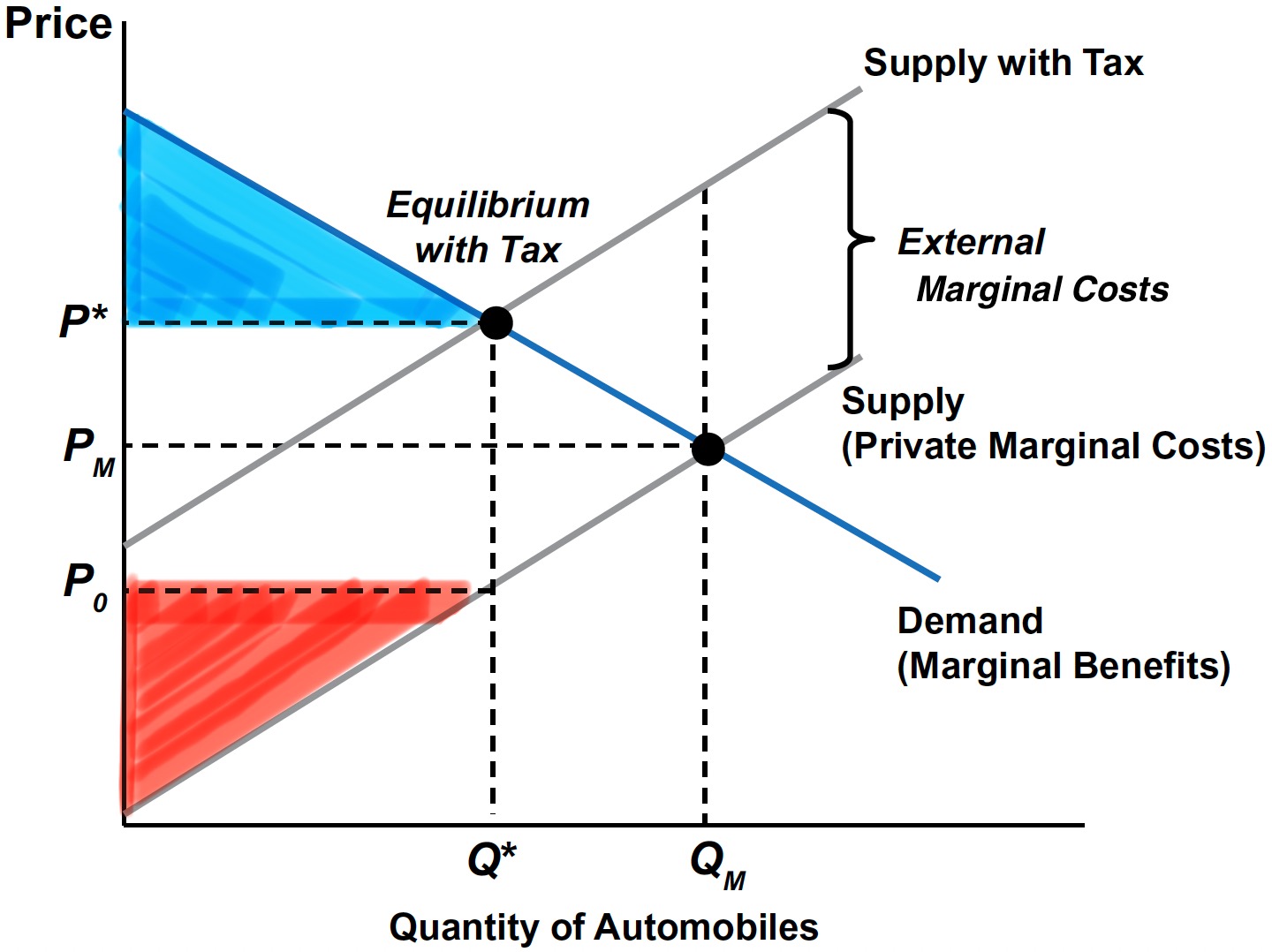

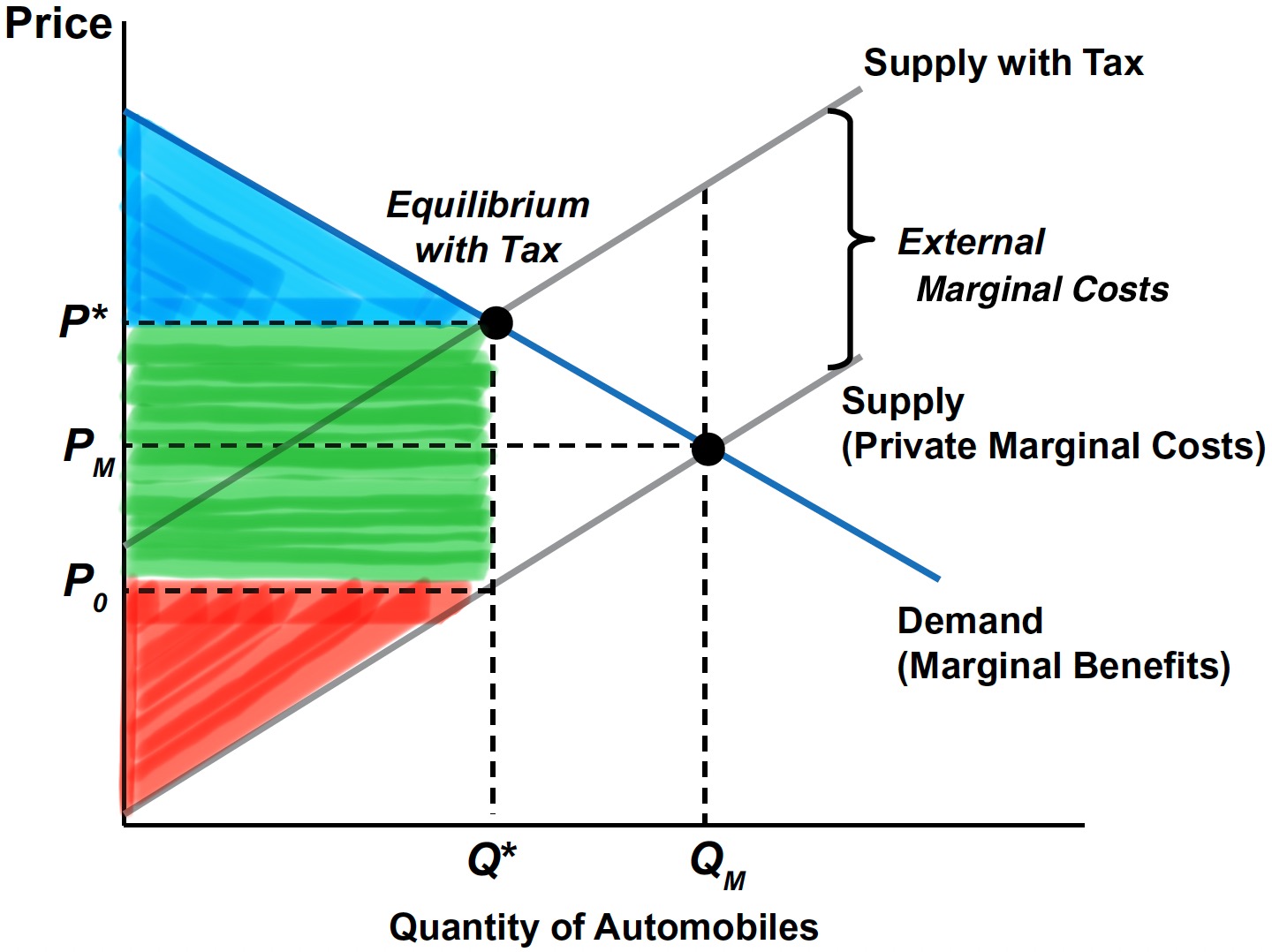

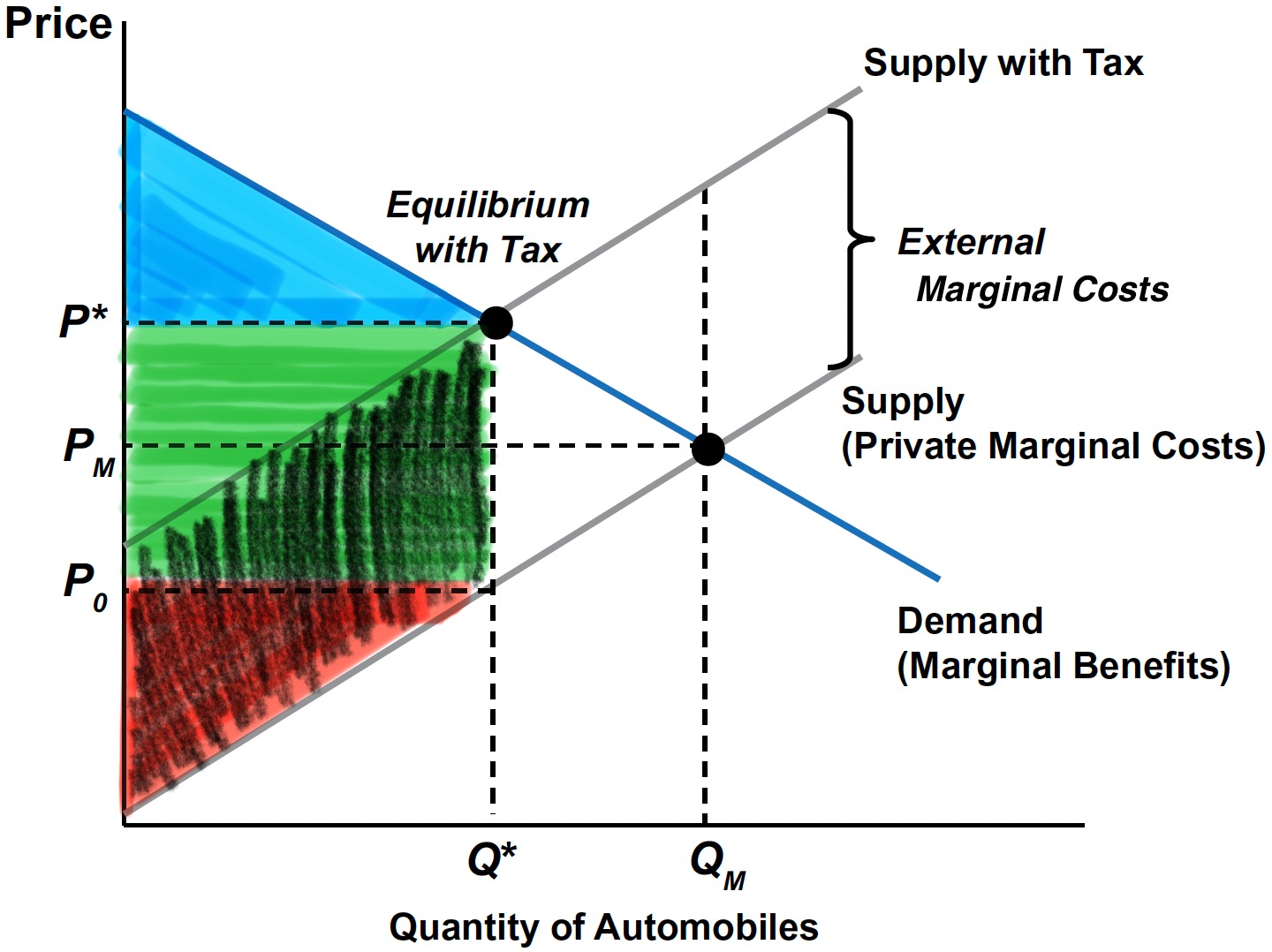

Welfare Analysis of the Automobile Market

- Consumer Surplus (CS): Area under demand and above price.

- Producer Surplus (PS): Area above supply (PMC) and below price.

- Without externalities, equilibrium maximizes CS + PS.

Welfare Analysis of the Automobile Market

Without Pigouvian Tax

Without Pigouvian tax, consumers and producers enjoys higher CS and PS than with the tax.

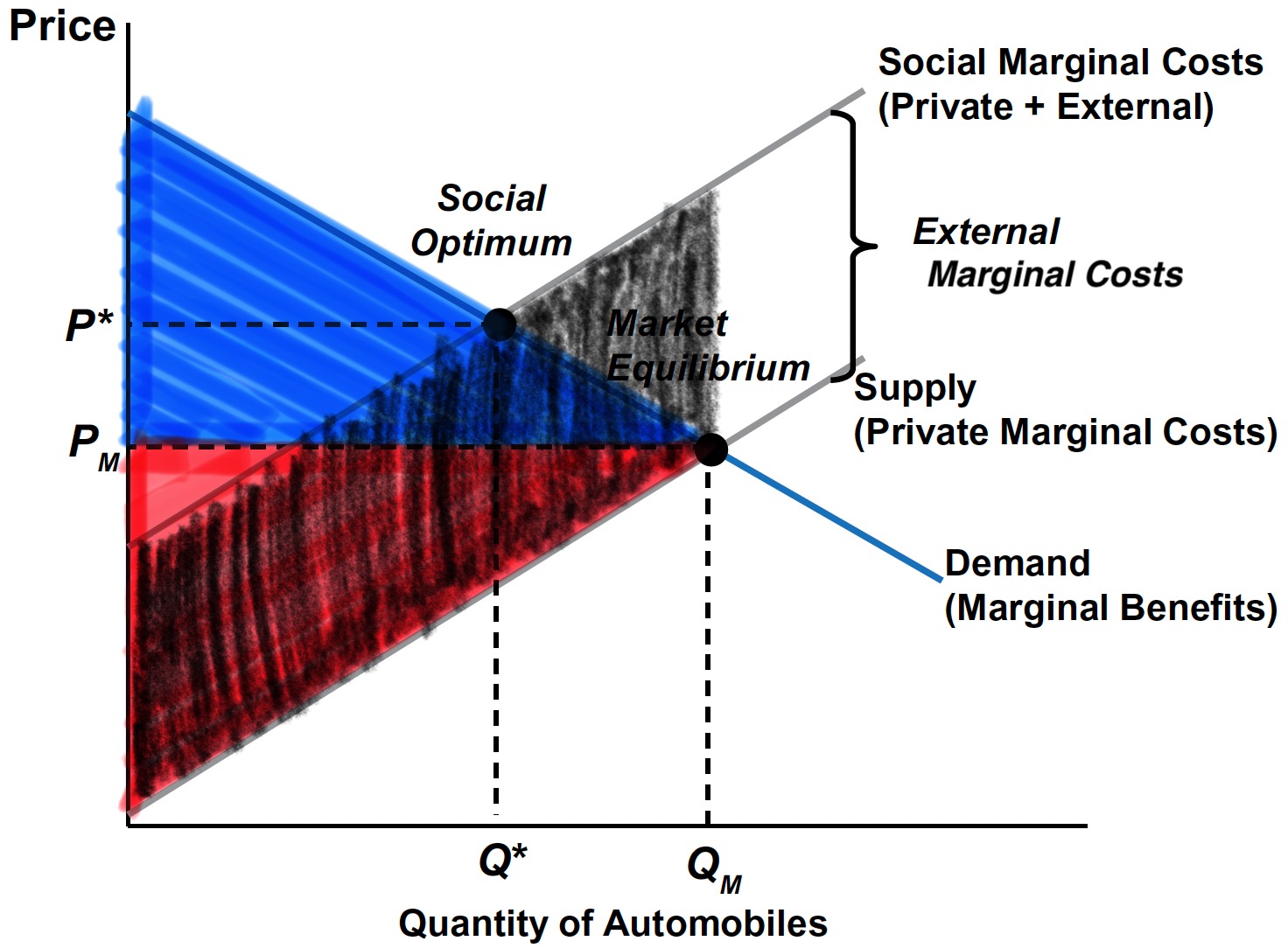

Welfare Analysis of the Automobile Market

Without Pigouvian Tax

However, these market activities impose a negative external costs to third parties, represented by the area between PMC and SMC up to the chosen quantity (\(Q_{M}\)).

Welfare Analysis of the Automobile Market

Without Pigouvian Tax

With such a negative externality, true social welfare (SW) is: \[ \begin{align} &\quad\;\; (\text{SW})\,=\, (\text{CS} + \text{PS}) \,-\, (\text{External Cost}). \end{align} \]

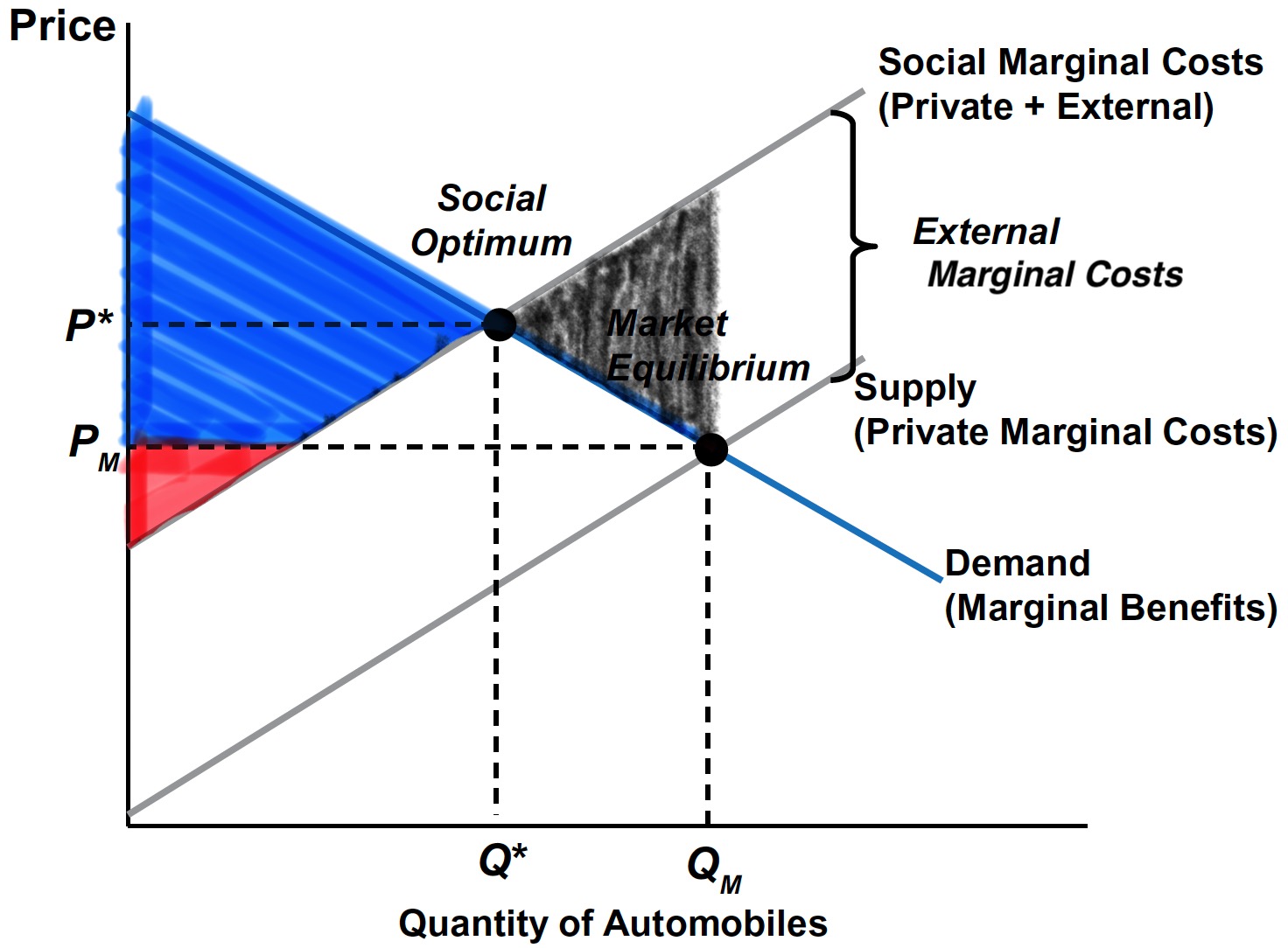

Welfare Analysis of the Automobile Market

Without Pigouvian Tax

Triangle C is the deadweight loss from overproduction where SMC > MB.

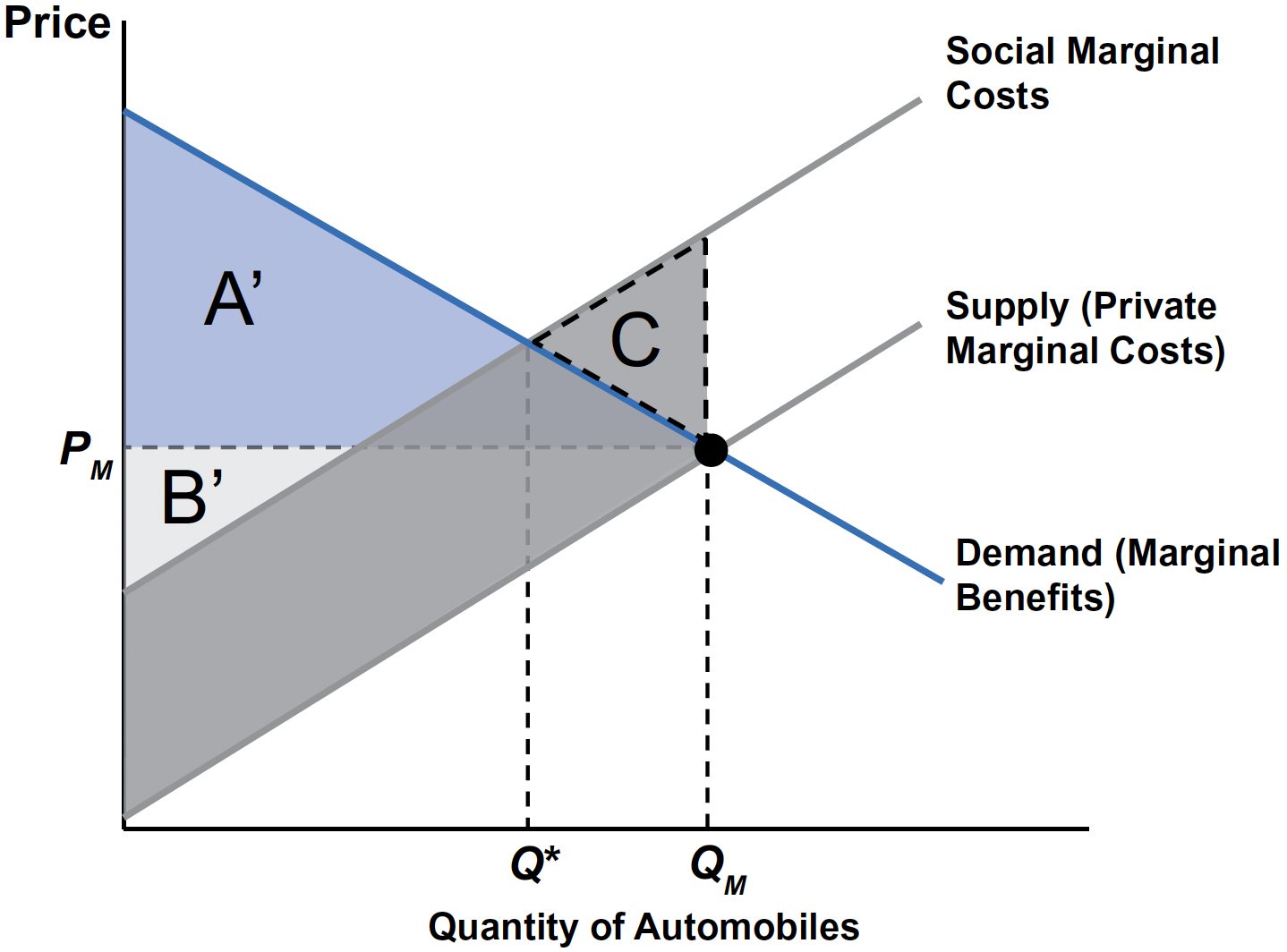

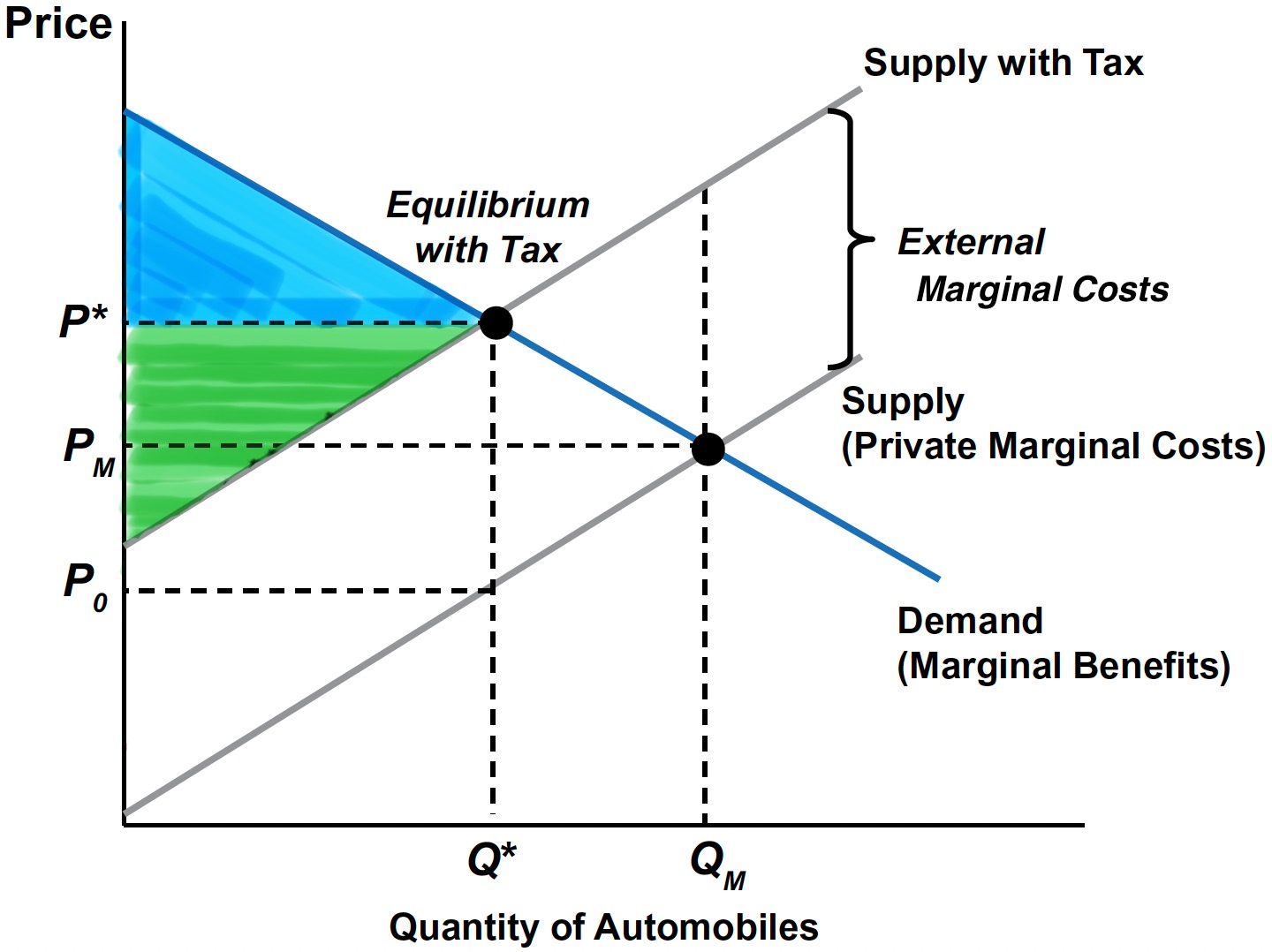

Welfare Analysis of the Automobile Market

With Pigouvian Tax

With Pigouvian tax, CS and PS are measured over quantities from 0 to \(Q^{*}\), the new equilibrium quantity.

Welfare Analysis of the Automobile Market

With Pigouvian Tax

Tax revenue equals \(t\times Q^{*}\).

Welfare Analysis of the Automobile Market

With Pigouvian Tax

Pigouvian tax caps external damage by shifting the market to the efficient quantity \(Q^{*}\).

Welfare Analysis of the Automobile Market

With Pigouvian Tax

With such a negative externality, true social welfare (SW) is: \[ \begin{align} &\quad\;\; (\text{SW})\,=\, (\text{CS} + \text{PS} + \text{Tax Revenue}) \,-\, (\text{External Cost}). \end{align} \]

- Pigovian Tax Improves Welfare: welfare rises by C relative to the unregulated outcome.

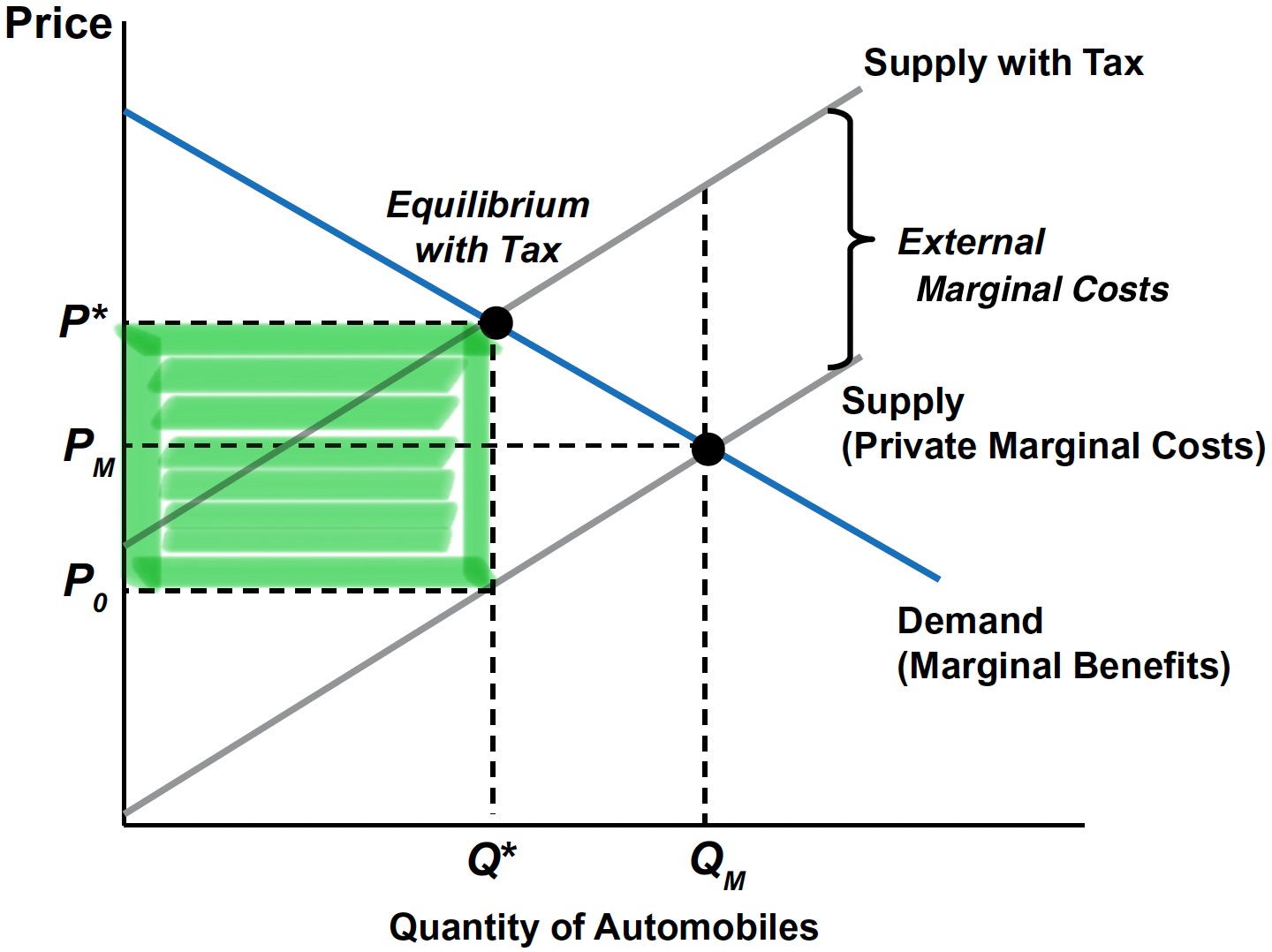

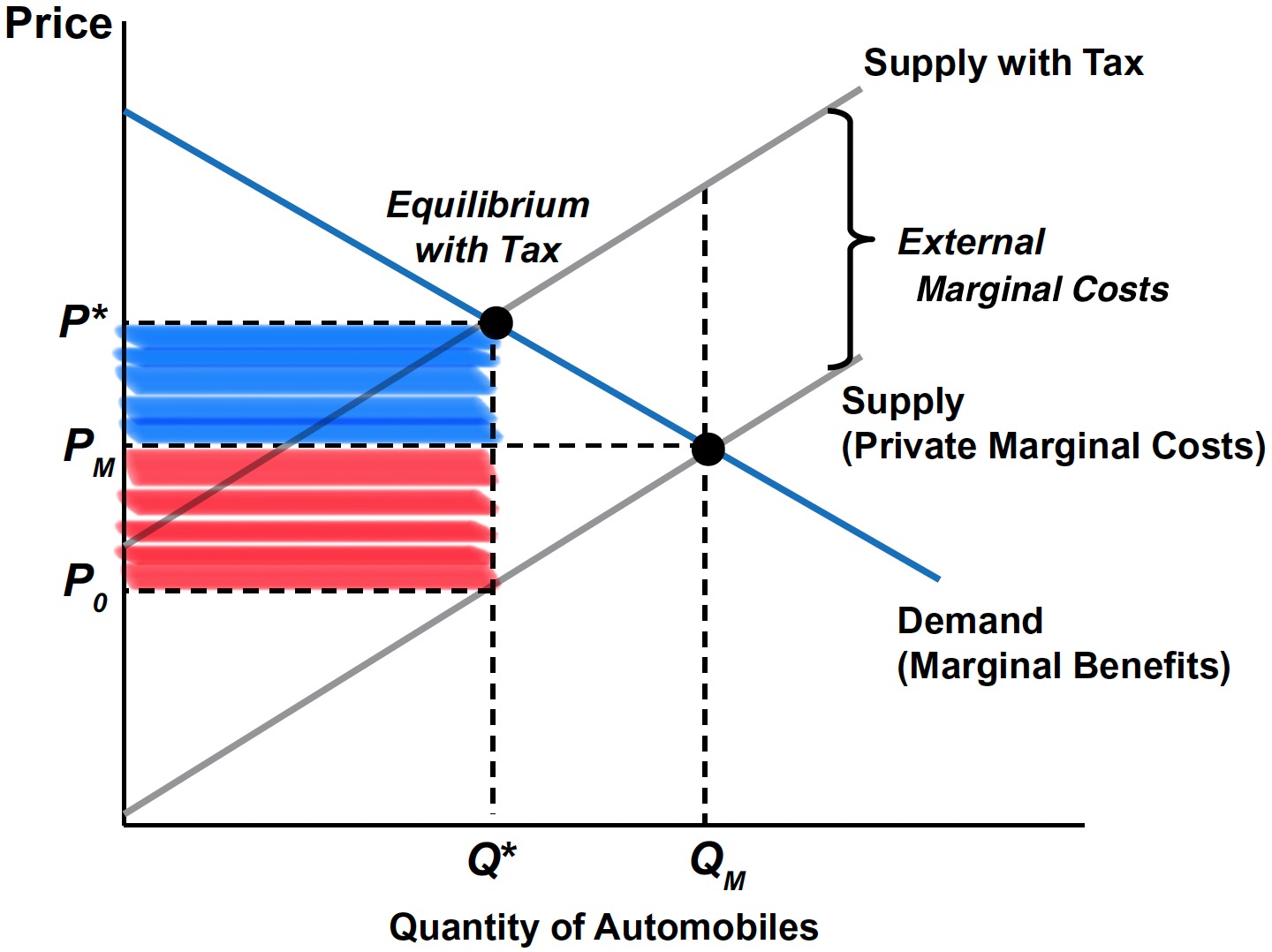

Tax Incidence

Tax Revenue: \(t \times Q^{*}\)

Tax incidence: The division of the tax burden between consumers and producers, determined by the relative elasticities of demand and supply.

Tax Incidence

Consumer incidence: The amount to which CS decreases, measured over quantities from \(0\) to \(Q^{*}\) \(\;\rightarrow\;\) Tax falls on consumers, who pay \(P^{*} - P_{M}\) more per unit.

Producer incidence: The amount to which PS decreases, measured over quantities from \(0\) to \(Q^{*}\) \(\;\rightarrow\;\) Tax falls on producers, who receive \(P_{M} - P_{0}\) less per unit.