Lecture 16

Climate Risk and Adaptation

December 1, 2025

What is Climate Risk?

Climate risk is the potential for adverse consequences for human and ecological systems, arising from the interaction of climate-related hazards with the exposure and vulnerability of people, ecosystems, and their biodiversity.

Source: IPCC (2022)

- Climate risk is not just about how big the storm or flood is.

- It comes from three ingredients:

- Climate Hazard – the physical climate event (heat waves, droughts, floods, storms)

- Exposure – who/what is in harm’s way

- Vulnerability – how fragile or resilient society and ecosystems are

\[ \boxed{\color{purple}{(\textbf{Climate Risk})} \;\propto\; \color{#1f77b4}{(\textbf{Climate Hazard})} \times \color{#17becf}{(\textbf{Exposure})} \times \color{#E69F00}{(\textbf{Vulnerability})}} \]

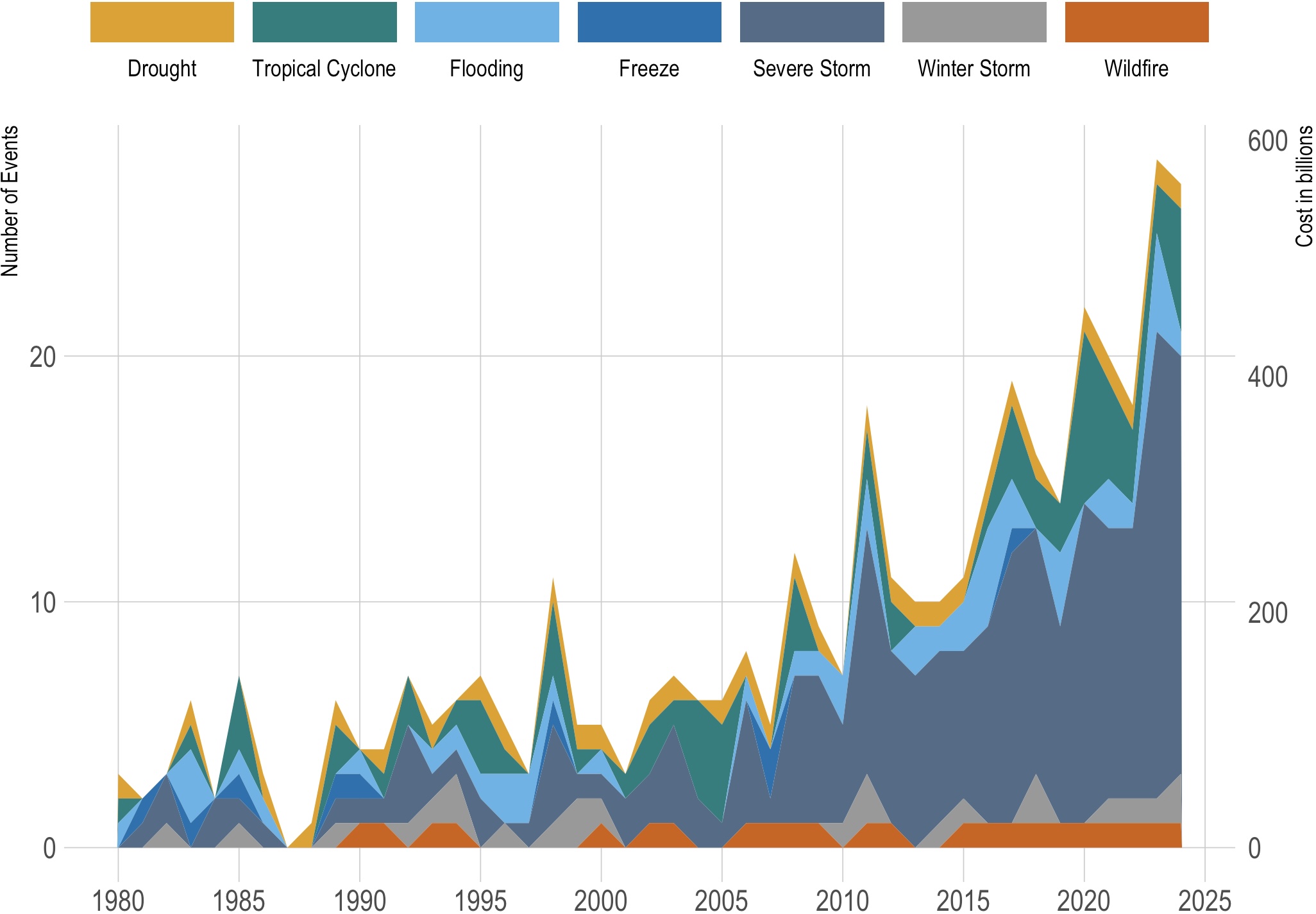

U.S. Billion-Dollar Weather and Climate Disasters

1980-2024 (CPI-Adjusted)

Source: Billion-Dollar Weather and Climate Disasters, NOAA (2024)

Why Flood Insurance Matters in the U.S.

Billion-Dollar Weather and Climate Disasters, NOAA (2024)

- Floods and storms: the most frequent and costly natural disasters in the U.S.

- Private insurance markets: historically reluctant to offer affordable coverage.

The National Flood Insurance Program (NFIP)

- Created: 1968 (National Flood Insurance Act)

- Managed by: Federal Emergency Management Agency (FEMA)

Basic idea:

- Provide flood insurance where private market is thin.

- Lower the need for emergency federal disaster assistance.

- Encourage safer building & land use in risky areas.

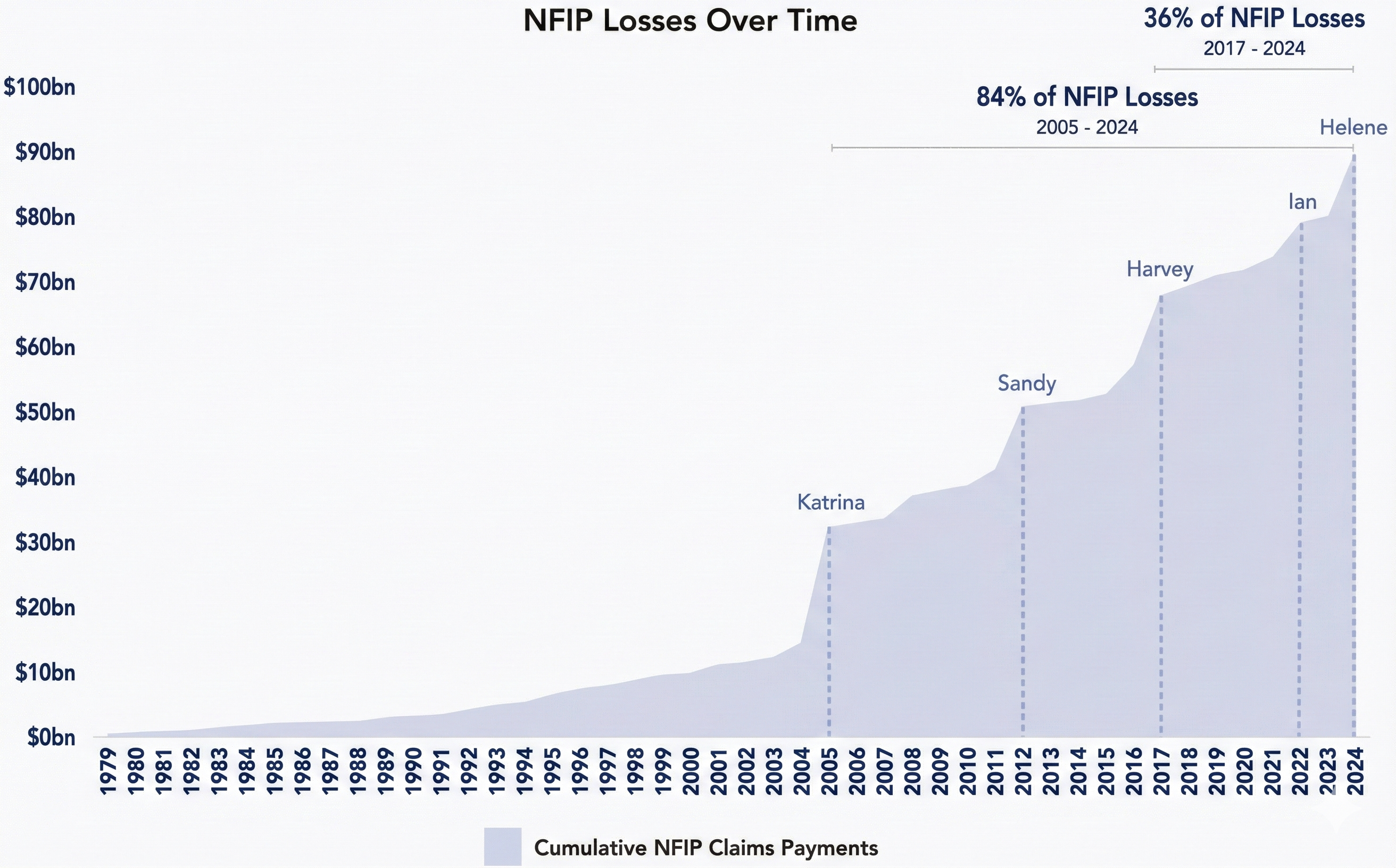

NFIP in Practice: Growing Claims Payments

- A small number of major hurricanes drive a large share of total claims.

- NFIP has repeatedly required Treasury borrowing.

- Outstanding debt reached roughly $22.5 billion (U.S. Government Accountability Office, 2025).

📈🌧️ Why Are NFIP Costs & Debt Rising?

Flood losses rise

when any of these increase:

\[ \boxed{ \begin{aligned} \color{purple}{\textbf{(Losses)}} &\;\propto\; \;\color{#1f77b4}{\textbf{(Climate Hazard)}} \\ &\qquad\times\; \color{#17becf}{\textbf{(Exposure)}} \\ &\qquad\times\; \color{#E69F00}{\textbf{(Vulnerability)}} \end{aligned} } \]

- Climate Hazard: stronger storms, heavier rainfall, sea-level rise

- Exposure: more development & repeated rebuilding in flood-prone areas

- Vulnerability: limited investment in infrastructure, rising construction and repair costs, legacy underpricing of premiums

It is a joint climate–economic–policy problem, not just a storm problem.

How FEMA Is Addressing Moral Hazard in NFIP

FEMA has already implemented several key reforms:

- Risk-based pricing (Risk Rating 2.0) – Premiums now reflect:

- Distance to water

- Flood frequency

- Elevation

- Distance to water

- Mitigation incentives – Premium discounts for:

- Elevation

- Floodproofing

- Compliance with updated building standards

- Elevation

- Repeated-loss controls

- Coverage limits and mitigation requirements after multiple claims.

- Community Rating System

- Better floodplain management (e.g., zoning, building codes, drainage, levees

, and other protective measures) ⇒ lower premiums for all residents.

, and other protective measures) ⇒ lower premiums for all residents. - Over 1,500 participating communities.

- Better floodplain management (e.g., zoning, building codes, drainage, levees

1. Myopia (Present Bias) in Flood Risk Perception

- Myopia (Present Bias):

Tendency to focus on immediate costs and heavily discount future benefits.- Up-front premium feels large; future flood loss feels distant.

2. Optimism in Flood Risk Perception

- Optimism:

Tendency to underestimate the likelihood of future losses.- Homeowners believe flooding is unlikely to happen to them.

3. Inertia in Flood Risk Perception

- Inertia:

Tendency to stick with the status quo under uncertainty.- Delay buying or renewing flood insurance.

4. Amnesia in Flood Risk Perception

- Amnesia:

Tendency to quickly forget past disasters.- If no recent flood has occurred, perceived risk declines.

5. Simplification in Flood Risk Perception

- Simplification:

Tendency to ignore complex or detailed risk information.- Overlook flood maps, probabilities, and damage estimates.

6. Social Herding in Flood Risk Perception

Tendency to base decisions on others’ behavior.