Lecture 28

Climate Change III: Adaptation

November 13, 2024

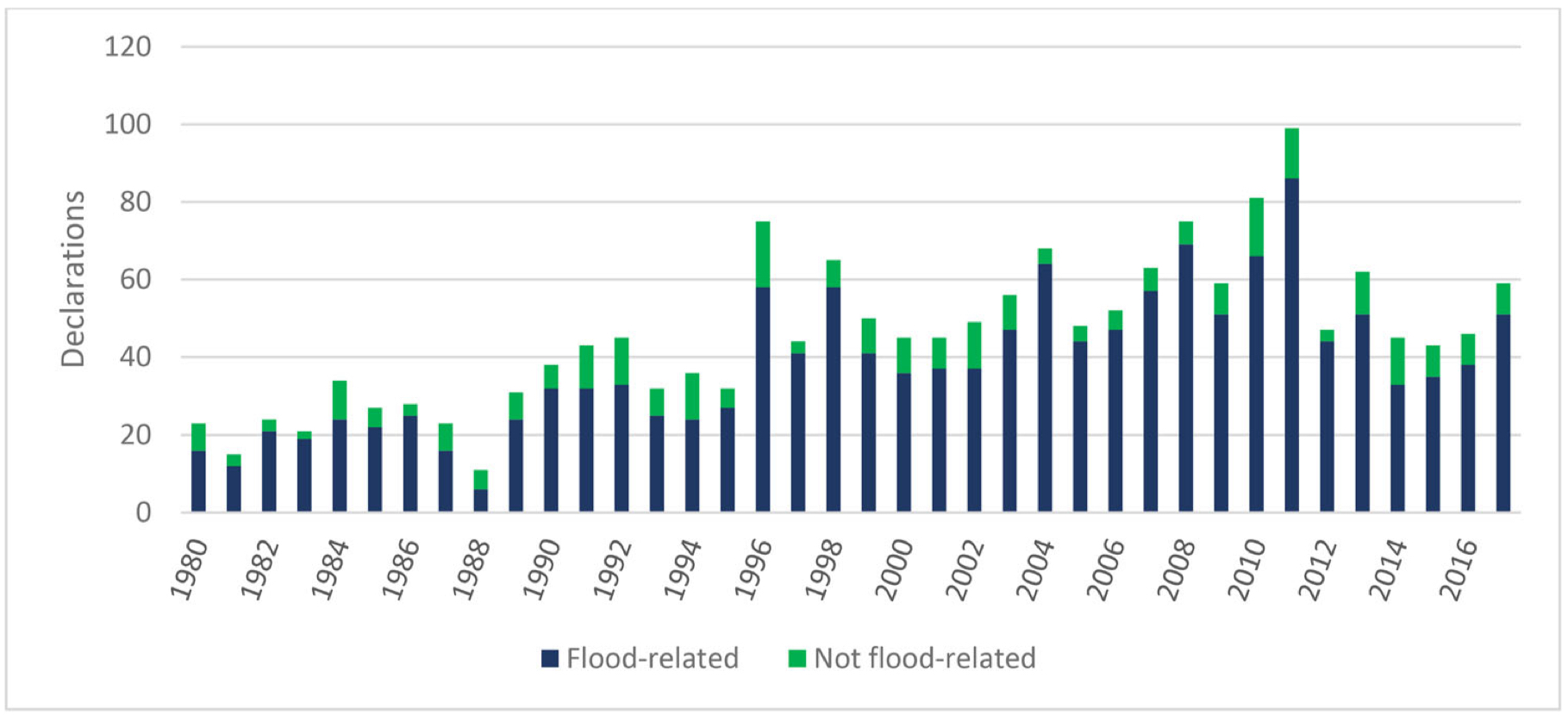

Flood Insurance in the United States

Major Disaster Declarations 1980 to 2017

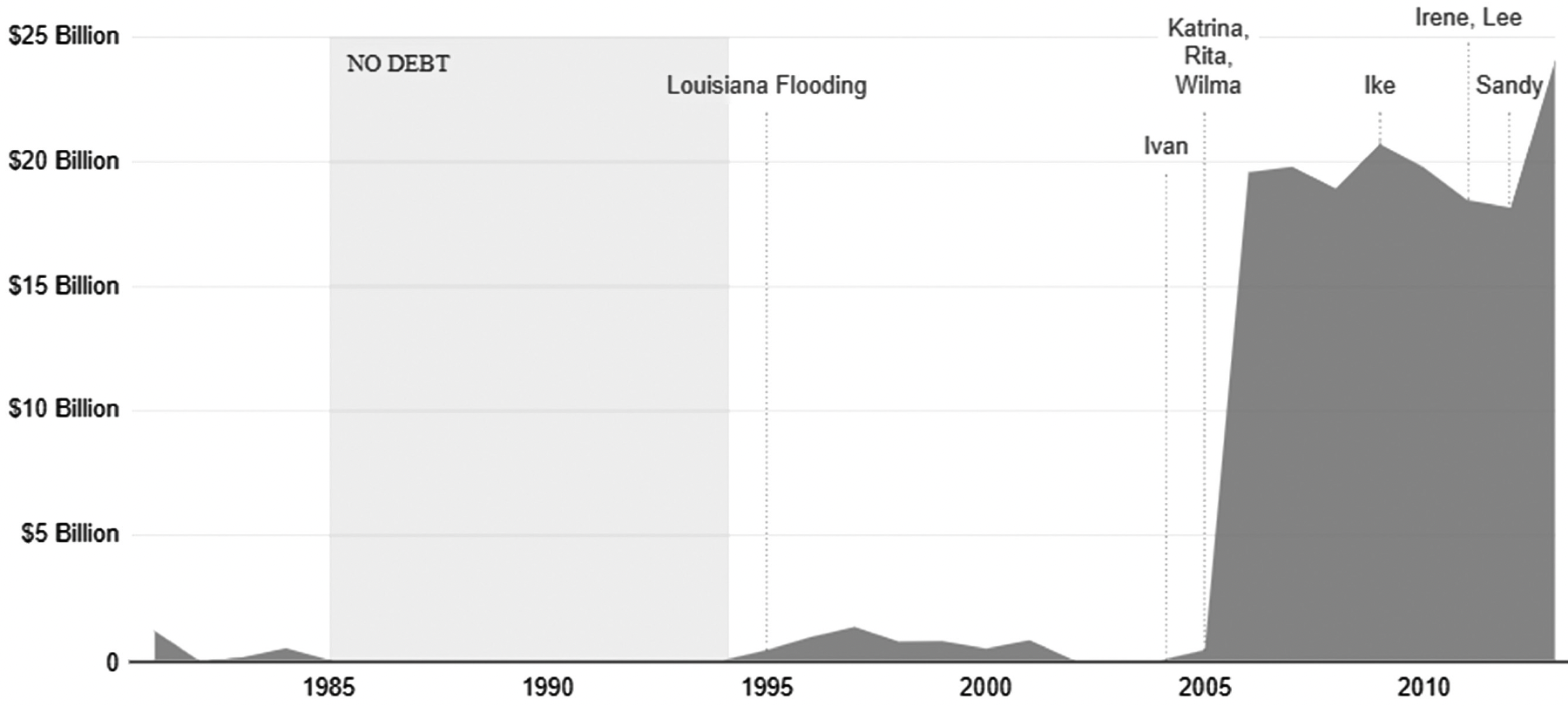

Flood Insurance in the United States

NFIP Debt

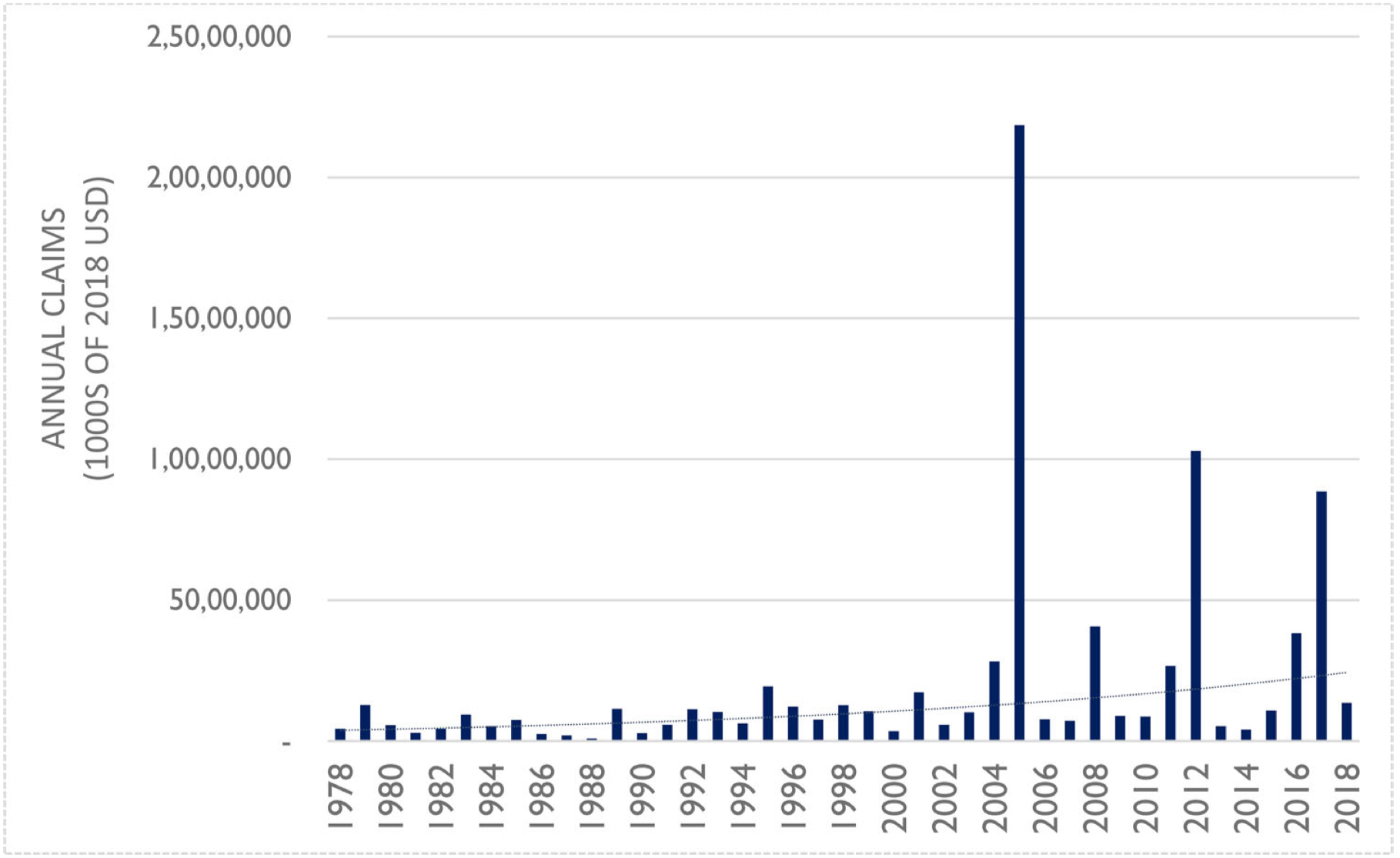

Flood Insurance in the United States

Total NFIP Claims Paid by Year (2018 values)

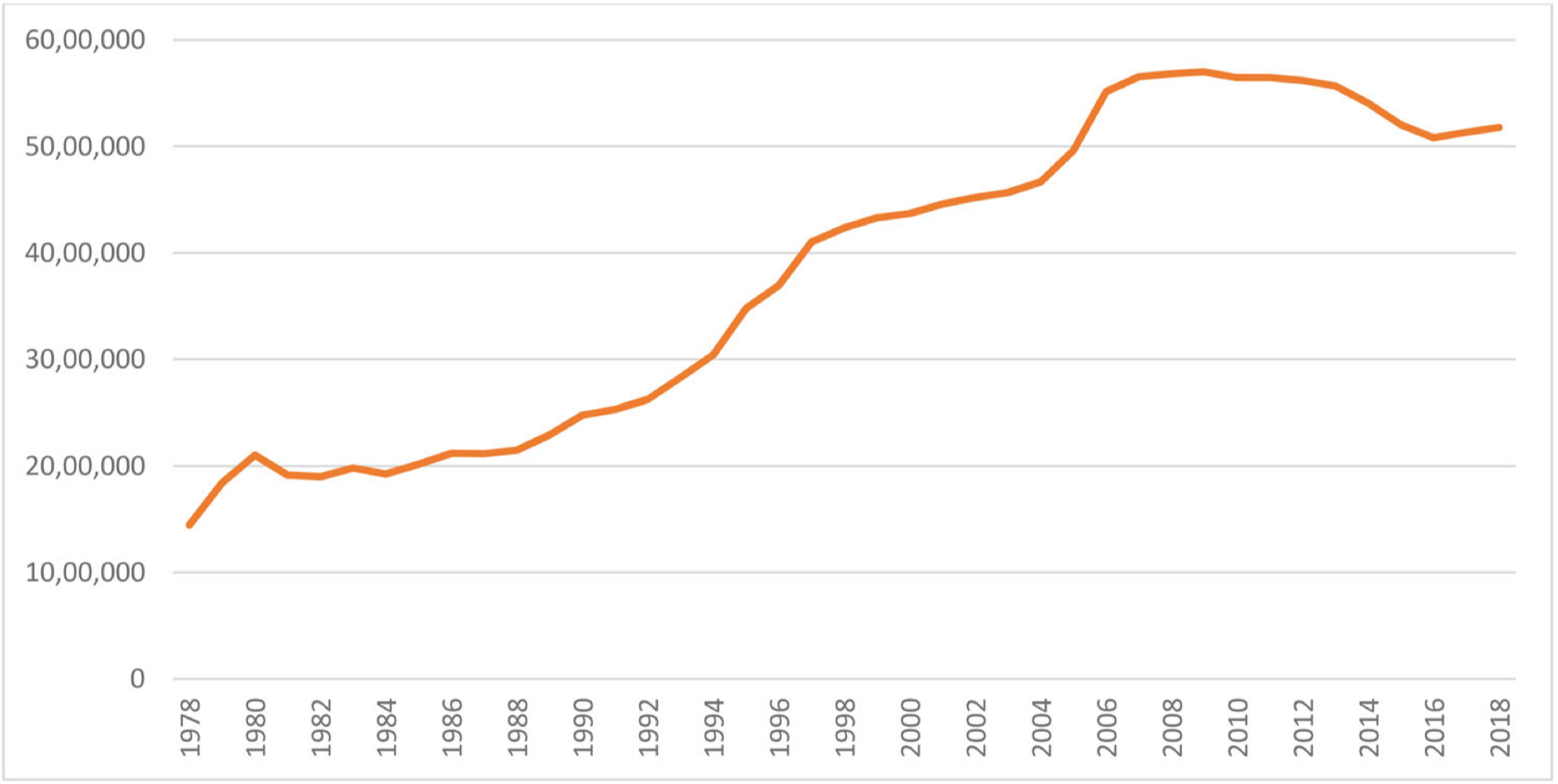

Flood Insurance in the United States

NFIP Policies-In-Force Over Time

Flood Insurance in the United States

Total Property Value

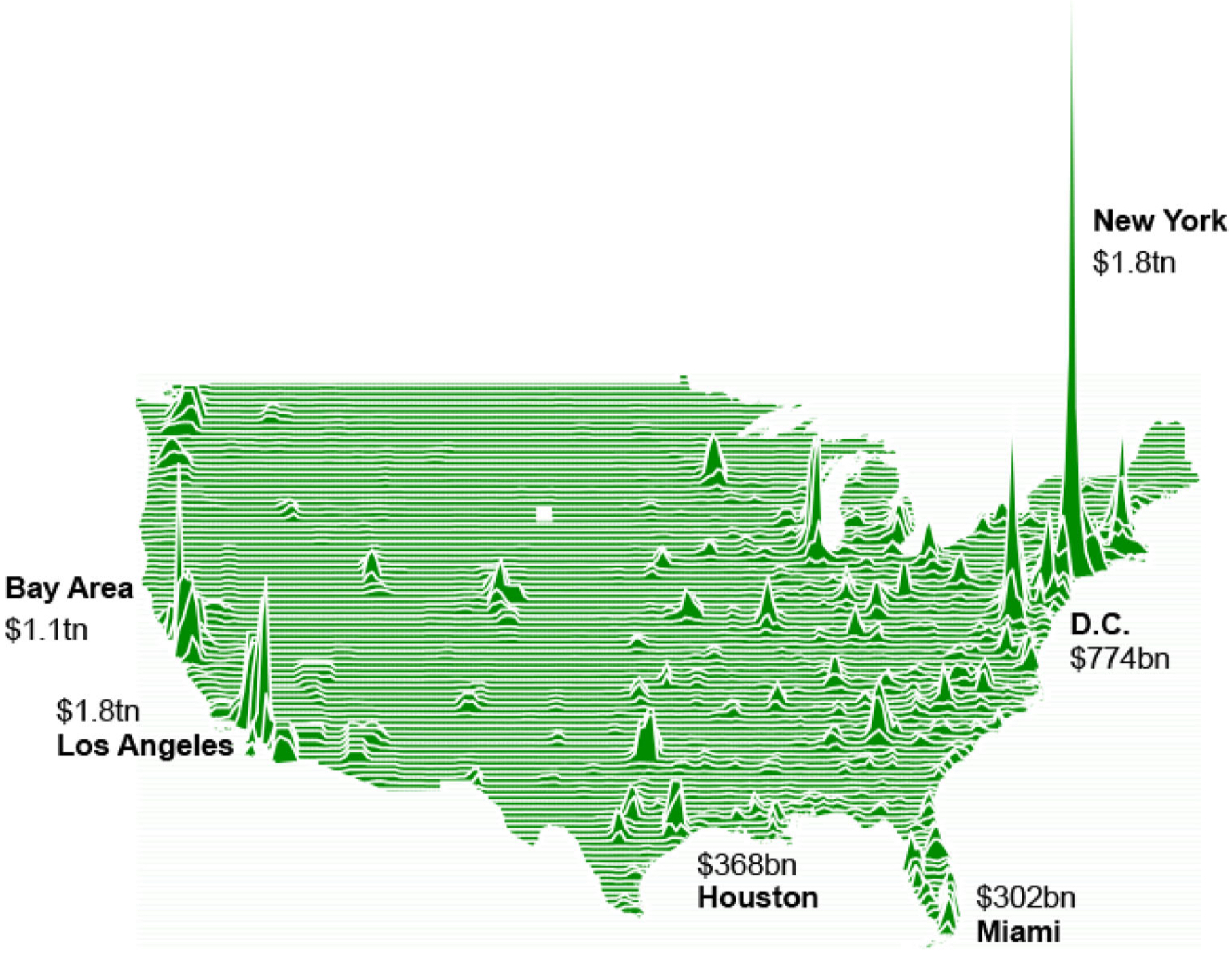

Flood Insurance in the United States

Top 30 Counties in the U.S. by the Number of NFIP Policies

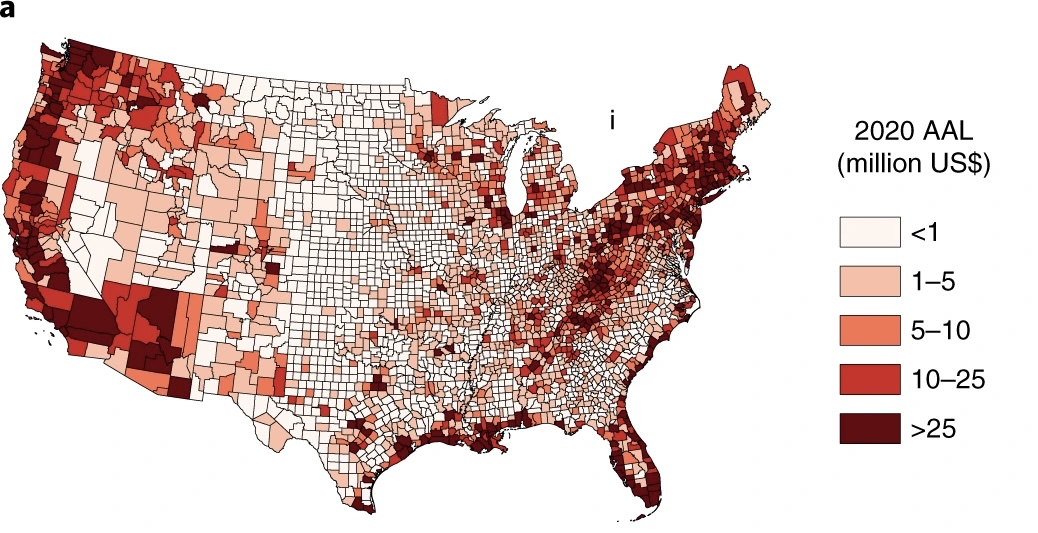

Flood Insurance in the United States

Average Annual Loss in 2020 (in $ million)

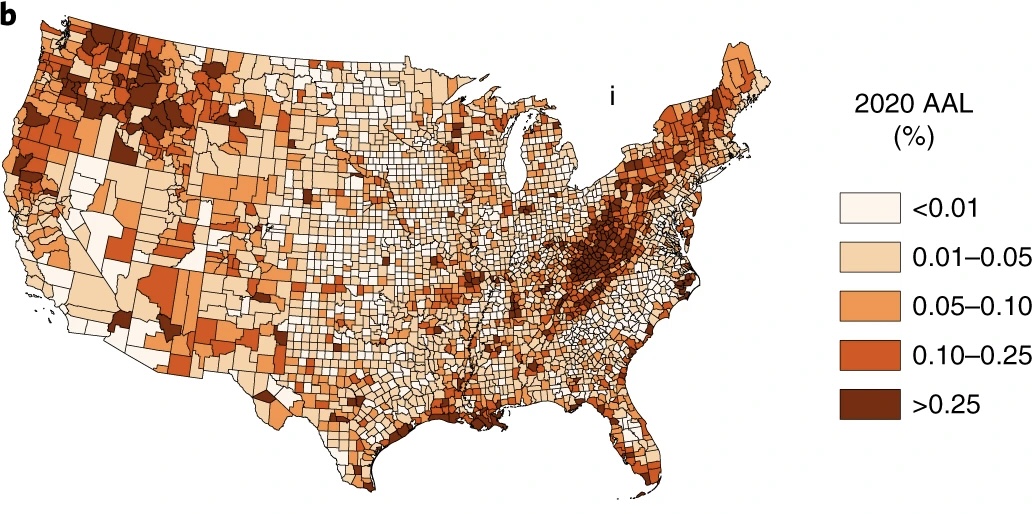

Flood Insurance in the United States

Average Annual Loss (AAL) in 2020 (in %)

Flood Insurance in the United States

Average Annual Loss (AAL) in 2020 (in %)

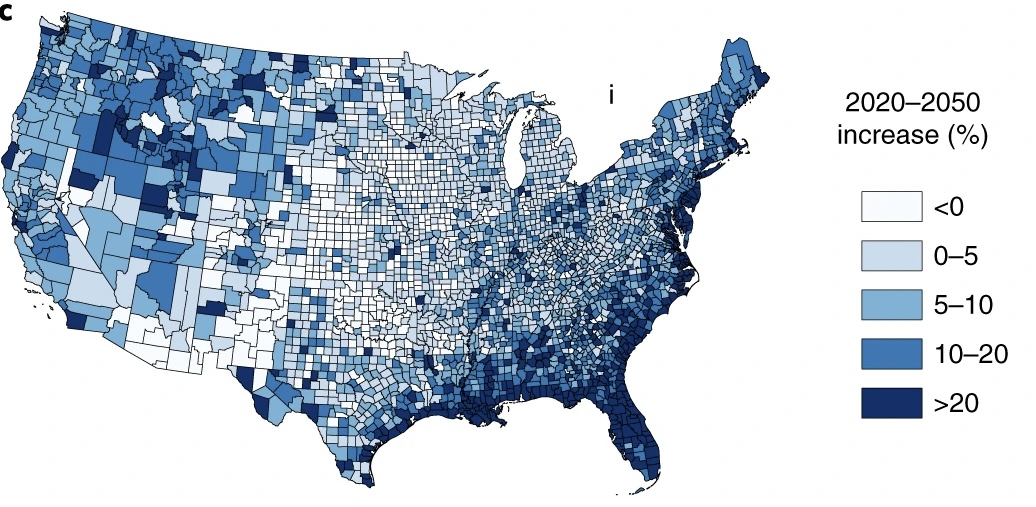

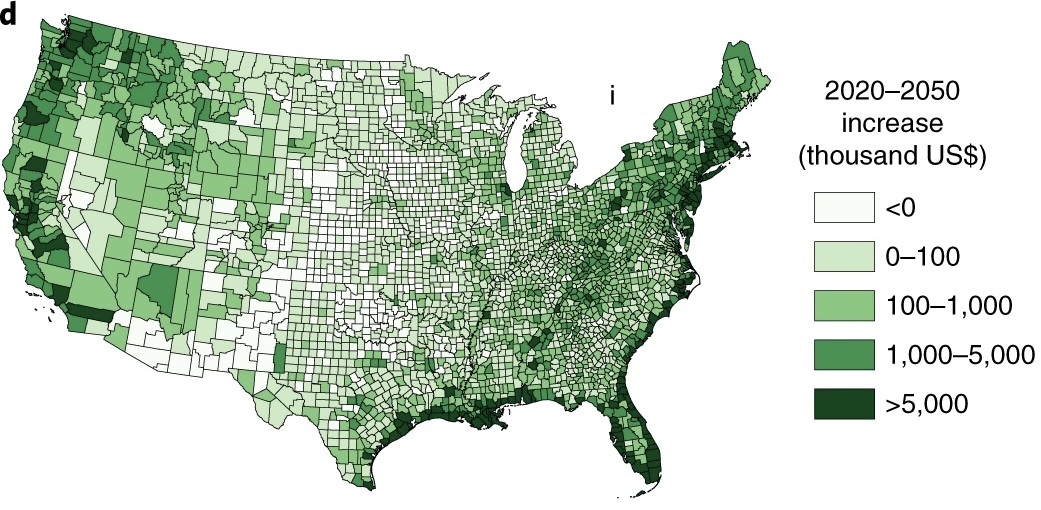

Flood Insurance in the United States

AAL Increase by 2050 (in $1,000)

Flood Insurance in the United States

Increase in Average Annaul Exposure to Flooding Due to Climate Change (in %)

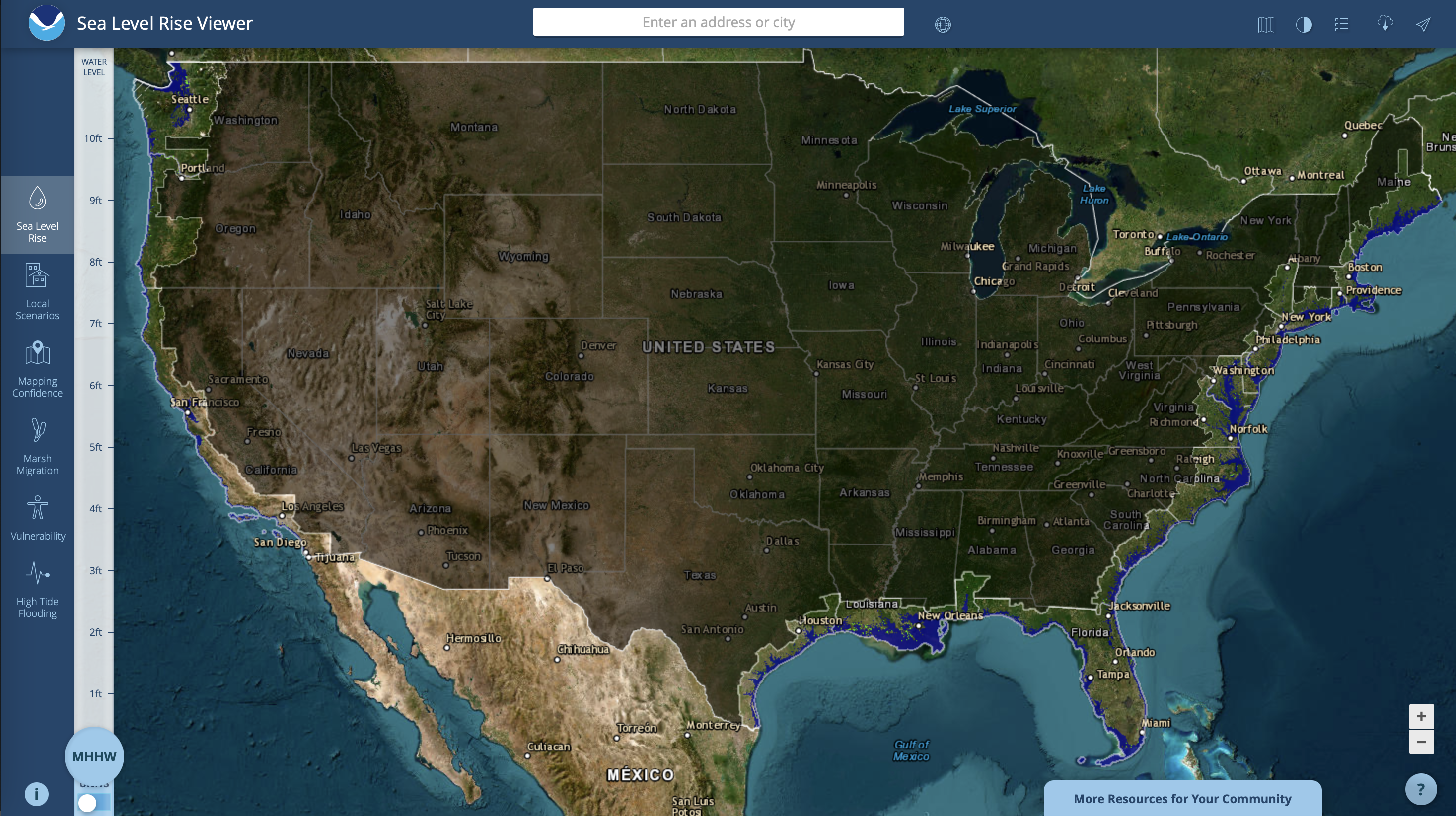

Sea Level Rise and Adaptation

NOAA Sea Level Rise Viewer

Sea Level Rise and Adaptation

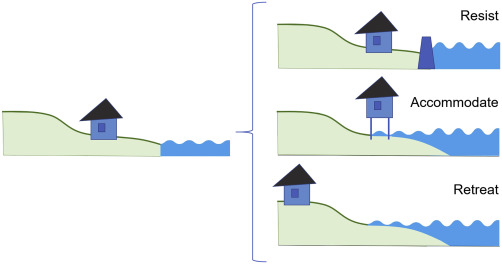

Adaptation Strategies for Sea Level Rise

1. Hard Infrastructure:

- Defensive Structures: Seawalls, bulkheads.

- Harden shoreline to prevent erosion.

- Costs:

- Expensive to build and maintain.

- Can disrupt natural ecosystems and neighboring properties.

Sea Level Rise and Adaptation

Adaptation Strategies for Sea Level Rise

2. Soft Infrastructure:

- Beach Renourishment:

- Adding sand to eroding beaches.

- Benefits:

- Maintains natural appearance.

- Provides temporary protection.

Sea Level Rise and Adaptation

Adaptation Strategies for Sea Level Rise

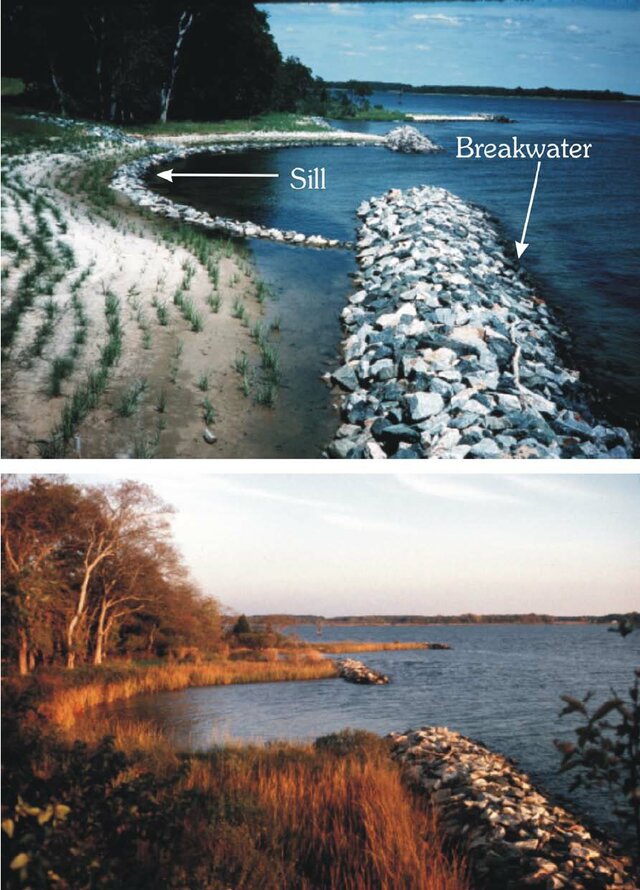

3. Green Infrastructure:

- Living Shorelines:

- Use of natural materials (plants, sand, rocks).

- Benefits:

- Enhances natural habitats.

- Cost-effective and sustainable.

- Requires maintenance and time to establish.

Sea Level Rise and Adaptation

Adaptation Strategies for Sea Level Rise

4. Managed Retreat:

- Relocation:

- Moving people and infrastructure away from high-risk areas.

- Challenges:

- Social and economic implications.

- Requires significant planning and resources.

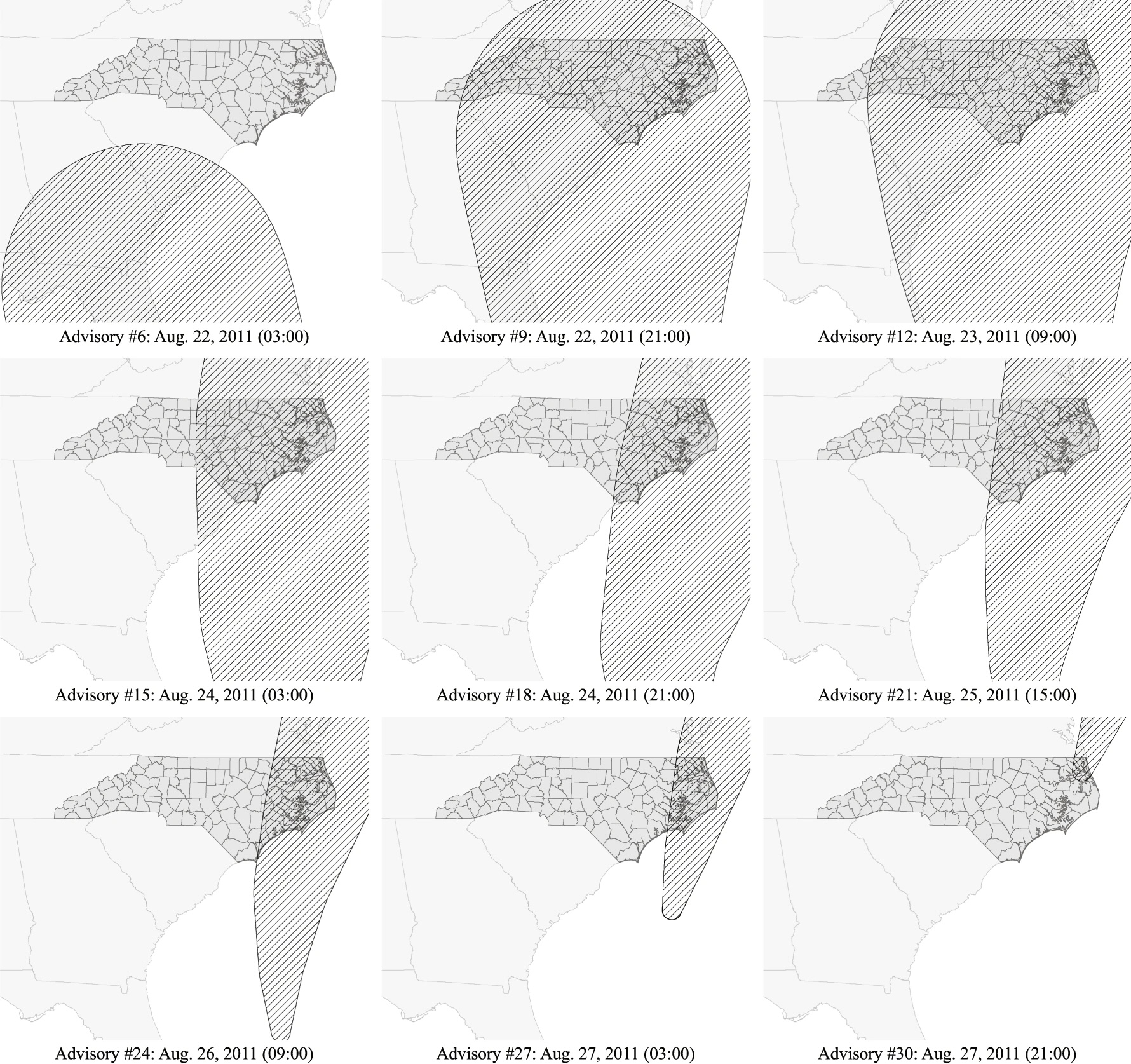

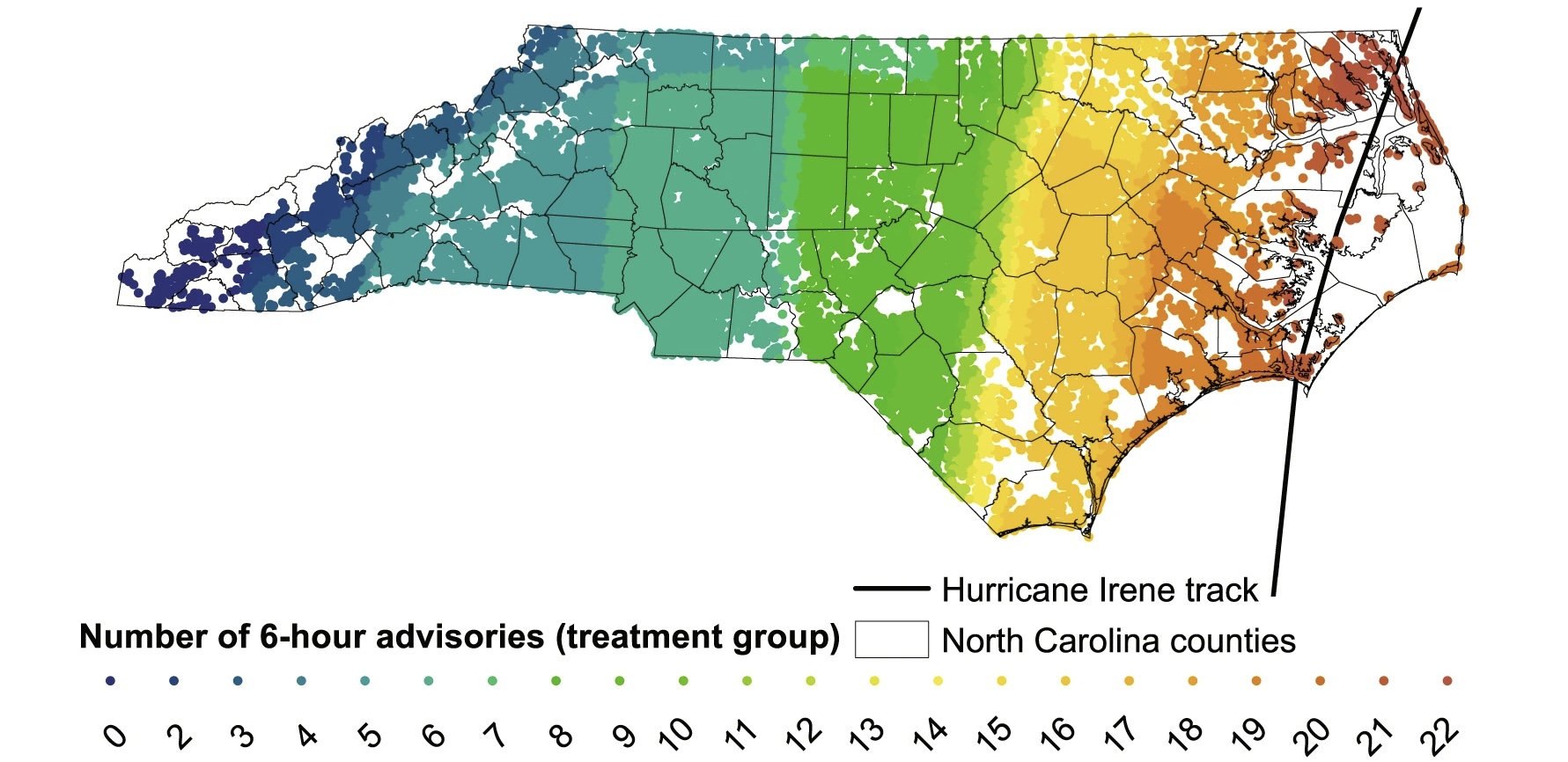

What to Expect When You’re Expecting a Hurricane

Effect of Time in the Cone of Uncertainty

- Even areas not physically impacted experienced negative birth outcomes.

- For every additional 6 hours spent in the cone, birth weights dropped by 4 grams.